The stock market rally ran into the wall of higher interest rates at the beginning of August. As a result, the market gave up their July gains and posted a -3.3%1 loss for the quarter. This was the first quarterly decline since the third quarter of 2022. Given the sharp upward turn in rates, the stock decline was actually rather modest; if investors truly believed the Federal Reserve would keep rates around 5.5% for the foreseeable future the decline probably would have been much worse. In other words, interest rates are driving the stock market right now, and not in a good way. The bond market also slipped into negative territory in aggregate last quarter, though many sub-sectors remained positive. As higher interest rates tend to compress earnings multiples, the high-flying NASDAQ gave back more (-3.9%) than the stodgier Dow Jones Industrial Average (-2.1%). That said, NASDAQ remains far ahead year-to-date. Unfortunately for small cap stocks, returns in this area (-5.2%) continued to trail all other domestic indices. Investors continue to favor larger, more profitable, and less leveraged companies.

International stocks also declined last quarter. Most foreign economies did not have the economic bounce in the third quarter that the U.S. did, so they didn’t see earnings estimates rise as much. Developed foreign economies were off -4.1%2 while emerging markets dropped -2.9%. India was a bright spot for emerging markets. Small company stocks in emerging markets did much better than larger ones; they recorded a surprising 2.9% gain. EM companies that focused on domestic demand did quite a bit better than those that rely on exports.

Bonds had another rough quarter. I’m going go into detail on the bond market in the Commentary section, so I will just say for now that last quarter’s -3.2%3 return wiped out all the year-to-date gain for the index. Nevertheless, several sectors posted a gain last quarter and are largely sidestepping the ongoing rout at the longer end of the high-grade market. 3-month T-bill yields are approaching 5.5% right now so money market yields are proving a strong alternative to bonds.

In terms of alternatives, gold also declined last quarter (-3.7%; don’t let anybody tell you that gold is an inflation hedge4). Since the dollar was strong due to America’s relative economic strength, gold went down in dollar terms. Real estate continues to be hurt by rising interest rates, but oil price gains led commodities higher.

Activity

The story of 2023 was supposed to be falling interest rates as the U.S. economy cooled, and strong foreign markets as the cooling U.S. economy dragged down the dollar. This is how the first quarter began, and that is how we positioned portfolios back then. However, by May that scenario had begun to collapse. The U.S. economy did not slow down, the Federal Reserve continued to hike interest rates, and foreign currencies slumped. All one can do is try to be among the first to recognize when the consensus forecast is wrong and update portfolio under- and over-weights accordingly. We believe that we did a very good job of reducing interest rate exposure on the bond side and underweighting income-oriented industries (utilities, real estate, etc.) on the stock side. We didn’t overweight technology as much as we might have because that industry historically suffers when interest rates are high. Just about all of the trades we made in September, and so far in October, have been designed to collect more current income (short term, floating rate bonds) or reduce net exposure to the high return sectors that would be high loss if bond yields keep rising.

Thought Experiment

If you want to understand the impact of higher interest rates on stocks, here is a thought experiment. Suppose there were three investors, Mr. Optimist, Ms. Practical, and Mr. Pessimist. They all have money in the stock market. Mr. Optimist hopes for 12% per year, Ms. Realist would be happy with 8% or 9%, and Mr. Pessimist says he’d be lucky to get 5%. Every so often Mr. Treasury Bill comes along and makes them an offer of a guaranteed return. The offer is usually around 2%, but sometimes the offer is as low as 1% and other times as high as 3%. Either way, the three investors always turn Mr. Treasury Bill down. In January, however, he offered them 4% guaranteed. Mr. Pessimist was sorely tempted – after all, 2022 was a bad year for stocks. When Mr. Treasury Bill came back in April offering 4.5%, Mr. Pessimist sold his stock and accepted the deal. “Maybe I’m getting a little less that I wanted”, he reasoned, “but I’m getting a guarantee”. He sold his stock. Mr. Treasury Bill came back again in July offering 5%, and now he is offering 5.5%. Ms. Practical is weighing the offer carefully. “You don’t often get the chance to lock in a yield this good”. The “Mr. Pessimists” are out of the market now. If the “Ms. Practical” out there begin selling…

Outlook

Simply put, interest rates are driving the financial markets. As long as they continue to rise, most stocks are going lower. Seasonally, however, markets tend to bottom out in October and post gains from October’s lows through the end of the year. I feel confident that when interest rates finally peak due to economic weakness and begin to head lower, we could see a surprisingly strong stock rally. I just don’t know how close we are to that “when”.

Source: Goldman Sachs Asset Management

I included this chart to show how well the biggest seven5 stocks have performed relative to the rest of the market. In the past when I have pointed out this discrepancy the point was to focus on the high and ultimately unsupportable valuation of that handful of technology-related stocks. Today I would prefer to focus on the other 493 stocks and how inexpensive all but maybe 15-20 of them have become. Additionally, I’d like to focus on how cheap stocks smaller than the top 500 are. Below is a ten-year chart of the U.S. stock market again separating large stocks, all stocks equally, and small stocks. Small stocks posted a 10-year compound return of 5.7345%. All stocks equally-weighted have a ten-year compound return of 7.5363%. There is no sense that the vast majority of stocks need some time to “cool down” after a strong decade of performance.6 The broad market is trading at February 2021 levels, while small caps have done almost nothing since August of 2018.

There are some very good reasons why smaller companies have under-performed, most having to do with lower profitability and higher interest costs. That said, there is a point in the business cycle where interest rates are falling in response to economic weakness and investors anticipate lower rates will stimulate demand. Early-to-midway through an economic recovery, almost all companies are profitable. In the interval between the anticipation of an economic recovery and the actual economic recovery, small cap stocks often more than double (2003-2006, 2009-2011, late March 2020 to early November 2021). I don’t know when the next cycle will begin, but the potential returns offered by the broader market, and small caps in particular, are very exciting.

Commentary

Since I have written a lot in this Quarterly Report about how important interest rates are, I’m going to devote the Commentary section to bonds and how they work. At their most basic level bonds are a contract between a borrower and a lender in which the borrower receives a sum of money and the lender receives a promise to repay the money plus an additional amount periodically to compensate them for two risks: 1) the risk that the principal when returned will have less purchasing power due to inflation than it did when the loan was made; and 2) the risk that the borrower is unable to pay back the full amount borrowed. The former is known as inflation or interest rate risk, and the latter is called default or credit risk. Today, let’s focus on interest rate risk.

If I buy a 5-year bond (in other words, make a loan) that yields me 4%, I’m going to receive $40 per year for every $1000 I invest. Let’s say one year later interest rates fall to 3%. Somebody wanting to buy a bond similar to mine at that point would only receive $30 per $1,000. If they saw that I was receiving $40, they might ask to buy my bond. I would sell that bond for more than $1,000 because I can’t get the same interest today as I could one year ago. Let’s say in year two interest rates go to 5%. I feel bad because I’m only getting $40 per year whereas a new issue buyer could get $50. If I go to sell my bond in order to buy the higher yielding bond, the buyer will not give me $1,000 because she would be losing out on $10 of income per year. Simply put, when interest rates go up, bond prices go down and when interest rates go down bond prices go up.7

Typically, the longer the time frame until a bond matures the greater inflation risk the buyer takes, so the more interest he expects to receive. Generally, two-year bonds yield less than five-year bonds which yield less in turn than thirty-year bonds, so a graph that represents bond yields over time is typically upward-sloping. That said, there are times when this relationship does not hold true. Today the Federal Reserve is holding short term interest rates unusually high in order to fight inflation. The bond market expects rates to begin to decline next year, so five- and thirty-year bonds yield less than two-year bonds. This is called an inversion. Inversions are usually regarded as signaling distress in the economy.

Under normal circumstances, the distress will play out promptly in the form of a recession, which will squash inflationary pressures and eventually allow the Federal Reserve to start lowering interest rates to stimulate the economy once again. So far in 2023 the distress has not been acute enough to cause a recession (perhaps because all of the monetary stimulus put into the system as a result of Covid shutdowns). In any event, interest rates have soared over the past two years such that bond investors have been crushed (unless they owned bonds have been short enough in duration that they matured before their future value could decline). Remember, if starting yields are low enough (ten-year bonds yielded around 1% at the beginning of 2021) and duration is high enough (7 years or so), bond yields rising from 1% to 5% over three years means you lose 25% (3 years of 1% interest) minus (4% higher yields times duration of 7; 3%-28%=-25%). Ouch.

This is a bigger loss than bond investors experienced at any point in the 1970s, because starting yields in the 1970s were much higher and therefore durations were somewhat lower. In fact, I’ve heard that the only worse period for U.S. bond investors was the late 1780s. Nobody’s retirement income projections planned for a 25% loss in bonds – it had never happened before in the modern financial era. That does not mean that it was unforeseeable. Longer term interest rates on the United States average closer to 4%. If one bought a bond in 2012 or 2016 or 2020 at a yield of less than 2%, one should have been aware of the loss potential if yields “normalized”. Mitigating loss potential would have involved underweighting duration and/or shifting a meaningful portfolio of one’s bond exposure to alternatives. We did both of these.

There are a couple of inferences I hope you will get from this Commentary:

• In bonds, low yields lead to low future returns. When the Fed forced interest rates below 2% after the Great Financial Crisis (2007-09), they created a bond market “bubble” that was going to pop at some point when yields came back to normal levels.8

• Bond yields are much higher now. Therefore, future bonds returns will probably be much better than they have been over the past 10-15 years. The math9 is much better for bonds today even if rates go higher since coupon rates are now high and duration is lower.

• Investors tend to see the recent past very clearly and the distant past very poorly, so they tend to position themselves to fight the last war and not the next one. The Fed tends to respond to investor fears even when they should know better.

It is hard to state how difficult it was to be a bond investor over the past decade, knowing that Federal Reserve policy meant that investors were being systematically underpaid for inflation risk. Today that is not the case. Many if not most sophisticated investors will tell you that bonds are more attractive than stocks today on a risk-adjusted basis, because bond prices fully reflect the new interest rate reality while many (larger) stocks still trade as if borrowing costs are going back to three or four percent. We anticipate shifting towards higher bond weightings in 2024, but we are always going to be nimble enough of thought to change our opinion if conditions warrant.

[1] Performance information from Standard & Poors, NASDAQ, and Dow Jones through NEPC. ↩︎

[2] Foreign market performance information from MSCI International through NEPC. ↩︎

[3] Bond performance from Bloomberg through NEPC. Gold performance through NEPC ↩︎

[4] Gold is a hedge against currency depreciation. If the dollar is strong, gold is not going to gain in dollar terms. ↩︎

[5] MAGMATN is Microsoft, Apple, Google (Alphabet), Meta (Facebook), Amazon, Tesla, and Nvidia. ↩︎

[6] It’s not like they were all that strong in the preceding decade (2001 to 2011) either. ↩︎

[7] If you want to get deeper into the mathematics of bonds, duration is a formula which calculates the principal gain or loss of a bond given a 1% change in its yield. The inputs are the bond’s coupon payments and the length of time to its maturity. A duration of 3 means that the bond’s price will change 3% for a 1% change in interest rates. The lower the coupon rate of the bonds and the greater the time until maturity (when you receive your principal back), the higher the duration. Higher duration bonds give you more total return than low duration bonds when interest rates fall, but when the rise higher duration bonds lose more. ↩︎

[8] The bond market tried in 2013 and 2018 to “slow leak” yields upward to avoid the pop that we eventually began to get in 2021, but the Fed capitulated both times to whining stock investors. ↩︎

[9] A 4% gain in yields over three years would produce a 9% loss (3 years times 5% coupon or 15%) minus (4 years times duration of 6 years or 24%). Duration is lower today because higher bond coupon payments mean more money (interest) comes back to the lender sooner. ↩︎

Disclosure

Past performance is no assurance of future results. Trademark Financial Management, LLC (“Trademark”) is a registered investment adviser with its principal place of business in the State of Minnesota. Trademark and its representatives are in compliance with registration requirements imposed upon investment advisers by those states in which Trademark operates. Trademark may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration. This newsletter is limited to the dissemination of general information pertaining to its investment advisory/management services. Any subsequent, direct communication by Trademark with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. A complete list of all recommendations will be provided if requested for the preceding period of not less than one year. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities in this list. Opinions expressed are those of Trademark Financial Management and are subject to change, not guaranteed and should not be considered recommendations to buy or sell any security. For information pertaining to the registration status of Trademark please contact Trademark at (952) 358-3395 or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov).

For information pertaining to the registration status of Trademark please contact Trademark at (952) 358-3395 or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov). For additional information about Trademark, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein or by calling 952-358-3395. Please read the disclosure statement carefully before you invest or send money. Any reference to a chart, graph, formula, or software as a source of analysis used by Trademark Financial Management staff is one of many factors used to make investment decisions for your portfolio. No one graph, chart, formula, or software can in and of itself be used to determine which securities to buy or sell, when to buy or sell them, or assist any person in making decisions as to which securities to buy or sell or when to buy or sell them. Any chart, graph, formula, or software used is limited by the data entered and the created parameters. The data was obtained from third parties deemed by the adviser to be reliable. Nonetheless, the adviser has not verified the results and cannot be assured of their accuracy.

Trademark Financial Market Update – August 23, 2023

1) The US dollar continues to rise, suggesting a “risk-off” approach for global markets (and risk assets in general). Beyond that, the period from the last ten days of August through the first three weeks of September tends to be very weak. Now, in any environment at least some sectors will perform decently but that said, there are environments in which investors should focus on loss reduction, not capital appreciation. These periods give you a chance to figure out what you’d like to own if the price was reasonable, and you wait for prices to fall into your range.

2) The upcoming summit at Jackson Hole, Wyoming (August 24-26) and Nvidia’s upcoming earnings announcement (August 24) are what is moving the market right now. On the former, the market wants confirmation that Fed chairman Powell would respond to declining inflation by cutting rates next year. Of course, Powell doesn’t want to promise anything. He has been largely successful in curbing inflation without causing a recession so far, so he is not likely to feel too concerned with Wall Streeters demanding lower rates. His “Achilles Heel” at this point is the financial sector. He doesn’t want to put any more stress on banks which are already reeling from higher deposit costs and the deteriorating value of their assets (loans, bonds, and mortgages written during lower yield periods). That is really the only thing that could force him to do something he doesn’t want to do. As for Nvidia, all I can say is that north of $460 (55 times next year’s earnings), its earnings and forward guidance need to be WAY better than expected.

3) I’ve been asked why bond yields are rising at the same time inflation is coming down. There are a couple of reasons:

• As of August 16th, The Atlanta Federal Reserve’s GDPNow model estimate for real GDP growth in the third quarter of 2023 is 5.8 percent, up from 5.0% on August 15th. This is way ahead of expectations and if it holds, absolutely prevents the Fed from cutting rates (lest inflation be re-ignited).

• The U.S. Treasury has increased the amount to be borrowed in upcoming Treasury auctions, especially at the longer end of the maturity spectrum, as a result of the growing debt and the cost of servicing it. Fitch downgraded U.S. government debt from AAA to AA+. It is likely that over time this means debt funding costs will rise, but more importantly, the more the U.S. government borrows, the less savings will remain for other borrowers to compete over. Since debt is usually priced at a spread over Treasuries (theoretically the safest debt), private borrowers will be forced to pay higher interest rates.

At the end of the day, it will be harder for rates to come down absent a real economic crisis, and any meaningful rate cut due economic weakness is unlikely to be maintained for long.

4.) The average Chinese stock is off just under -13% this month. This is twice the average loss of EM ex-China. Latin America is down -7%, but India is only off -2.5%. Europe is off -5.5% and Japan -5%. Global investment composites may well be underweight India, given its growth and strong relative performance.

5.) We keep being told by investment strategists that high yield debt is unattractive because spreads over Treasuries are on the narrow side historically and the economy is bound to deteriorate under the weight of high interest rates and reduced Fed liquidity. Meanwhile, high yield and floating rate below investment grade debt continue to over-perform dramatically. The iShare High Corporate Bond ETF, HYG, is up 4.20% YTD, while AGG has gone negative (-0.04%).1 If high yield bonds are essentially a hybrid of stocks and bonds, in this environment high yield debt may, and probably should, draw money away from both bonds and stocks.

[1] As of market close on 8/22/23. Source: YCharts.com ↩︎

Disclosure

Past performance is no assurance of future results. Trademark Financial Management, LLC (“Trademark”) is a registered investment adviser with its principal place of business in the State of Minnesota. Trademark and its representatives are in compliance with registration requirements imposed upon investment advisers by those states in which Trademark operates. Trademark may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration. This newsletter is limited to the dissemination of general information pertaining to its investment advisory/management services. Any subsequent, direct communication by Trademark with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. A complete list of all recommendations will be provided if requested for the preceding period of not less than one year. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities in this list. Opinions expressed are those of Trademark Financial Management and are subject to change, not guaranteed and should not be considered recommendations to buy or sell any security. For information pertaining to the registration status of Trademark please contact Trademark at (952) 358-3395 or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov).

For additional information about Trademark, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein or by calling 952-358-3395. Please read the disclosure statement carefully before you invest or send money. Any reference to a chart, graph, formula, or software as a source of analysis used by Trademark Financial Management staff is one of many factors used to make investment decisions for your portfolio. No one graph, chart, formula, or software can in and of itself be used to determine which securities to buy or sell, when to buy or sell them, or assist any person in making decisions as to which securities to buy or sell or when to buy or sell them. Any chart, graph, formula, or software used is limited by the data entered and the created parameters. The data was obtained from third parties deemed by the adviser to be reliable. Nonetheless, the adviser has not verified the results and cannot be assured of their accuracy.

Schwab Transition

In 2020, our custodian, TD Ameritrade, was acquired by the Charles Schwab Corporation. Over the past several years, the two companies have put tremendous thought and resources into planning and preparing for the transition of TD Ameritrade clients over to Schwab’s custody and technology platforms. The final transition is scheduled for the first weekend in September 2023 (Labor Day weekend), at which time all your accounts will be transitioned from TD Ameritrade to Schwab. At that time, you will receive new Schwab-based account numbers for the accounts we manage. We are happy to report that you will not need to sign any new paperwork. The Schwab and TD Ameritrade teams have worked hard to make this transition as smooth as possible. In these coming months, you should expect to receive more communication from Schwab, TD Ameritrade, and Trademark regarding the transition. Please feel free to contact us at any time if you have questions.

Summary

The second quarter of 2023 was not that different from the first quarter. Stocks continued to surge despite forecasts of recession and a hawkish Federal Reserve because investors continued to believe that any economic downturn would be milder than predicted. First, April brought better than expected corporate earnings announcements. Then, May brought news that unemployment was holding steady in the 3.6%-3.7% range while the tide of inflation continued to recede. When the news is better than what is priced into stocks and there is a great deal of money parked in money market funds because of 2022’s volatility, this “recipe” produces higher prices as investors rush to get back in.

U.S. Stock Market Performance, 2Q23

If the story of the first quarter was the unveiling of ChatGPT and the artificial intelligence (AI) mania it unleashed, the story of the second quarter was semiconductor chip maker Nvidia’s profit announcement on May 24th, in which profit guidance tripled. For AI stocks, this added gasoline to the fire. The NASDAQ, where most of such companies reside, rose 13.07%1 during the quarter. The S&P 500, increasingly a technology index, rose 8.74%. The average company rose only 3.87%, however2 (most companies are not, strictly speaking, technology companies). The small stock-oriented Russell 2000 gained 5.21%. The Dow Jones Industrial Average rose 3.89%. The underperformance on the part of large tech stocks in 2022 was fully recovered by quarter end; both they and the slower growing, high dividend stocks of the Dow were roughly 12% below their year-end 2021 levels at quarter end3.

International stocks did far less well in the second quarter than they did in the first. Foreign stocks prefer a weaker U.S. dollar and low inflation, and they got neither. Still, with recession largely avoided thus far and the hope for interest rates to come down later this year, foreign markets added 2.95%4 last quarter. Japan led the way in developed markets with a 7.24% gain; the global move to technology and robotics plays into their strength. On the emerging market side, while the index itself gained only 0.90%, Latin America roared ahead 14.05%. Latin American central banks have been the first in the world to see inflation fall enough to begin cutting interest rates. Asia ex-Japan lost -1.26% on the disappointing (so far) recovery in China.

As a whole, bonds lost money during the second quarter. Their -0.84%5 decline reflected the fact that the economy has not slowed as much as forecast and as a result, the Federal Reserve is still raising interest rates. Of course, the bond market is as diversified as the stock market is, so certain types of bonds gained in value last quarter. Both ex-U.S. developed market bonds and emerging market bonds rose last quarter, as did U.S. corporate high yield bonds and floating rate debt. The key was to take on credit risk but not interest rate risk. Default risk fell during the quarter, but interest rate risk did not. One could have avoided both types of risk and earned 1.22% in short term T-bills.

Activity

As the economic data came in during the quarter that continued to show that economy was not in fact on the cusp of recession, risk appetites grew, and we needed to nudge portfolios away from the defensive, dividend-oriented value funds that we started the year with. We increased exposure to cyclical and growth sectors with the proceeds from value fund sales and from cash, which had built up somewhat last year. We have also sold most positions that are “market neutral,” meaning they aim to provide single-digit returns no matter what the overall stock market is doing by using arbitrage, options, or some other hedge-type strategy. They were attractive in 2022, but by late-May it was becoming obvious that hedging was not going to be necessary.

Outlook

Three months ago I was tentatively optimistic that we could have a pretty good year despite the threat of recession looming, because investor sentiment was weaker than it objectively should have been6. Today, with stocks being roughly ten percentage points higher, I feel we have mostly played out the “sentiment reversal” trade, such that future gains are going to be harder to come by. I believe momentum and positive inflation news will carry us for maybe another month or so, but September is seasonally rough7, and year-over-year inflation comparisons start getting tougher by autumn. The stock market has already digested the likelihood of a 0.25% interest rate hike on July 26, but it expects that bump to be the last one. If it begins to look like they will hike again in September, we could have some turbulence. The key for markets going forward is maintaining the current “not-too-hot, not-too-cold” environment where unemployment stays below 4% but prices and wage growth are closer to 3% than 4%. Again, I think we can do that in the short run.

Commentary – The S&P 500 is a Bad Benchmark

This Commentary is sub-titled, “How come the S&P 500 is up 15% and I’m only up 8%?” The answer to this question goes to the nature of the S&P 500 as a benchmark. A benchmark is designed to represent what percentage return an average investor in a particular asset category should have expected to receive. Therefore, it obviously follows, the benchmark should be broad enough to cover most of the asset category it is supposed to represent, and it should be investable – meaning the benchmark return was achievable through easily purchased securities. For these reasons, benchmark makers (Standard & Poors, Dow Jones, Bloomberg, etc.) make adjustments to a simple size-weighted model. Stocks that are hard to purchase because fewer shares trade are usually excluded from benchmarks, as are companies with dual share classes.8

Over the years, some benchmarks have proven to be less than ideal because of structural changes. For example, in 1990 Japanese stocks were the lion’s share of the international stock benchmark (MSCI). Before the Japanese asset bubble burst, this international index owned more Japanese stocks than all the other non-U.S. countries combined. Almost all active international managers under-performed the benchmarks from 1985 through 1989. After the Japanese bubble burst, international fund managers routinely outperformed the benchmark by underweighting Japan. This worked for about 25 years. U.S. investors experienced a similar situation during the dot.com bubble. The initial public offering of Netscape in 1995 (think AOL) sparked a mania that lasted until March of 2000. The S&P 500 was brutal to try to beat between 1995 and 1999, then surprisingly easy to beat from 2000 to 2008 as over-ownership of tech stocks was bled out of the market. The question you might be asking at this point is, how do prices get so out of line?

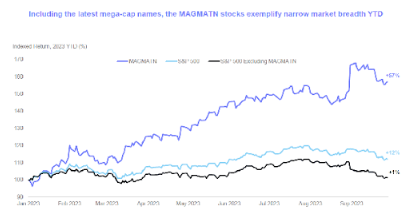

The S&P 500 is the most widely accepted benchmark because it covers more than 85% of the U.S. stock market capitalization, which is dramatically more than the Dow Jones Industrial Average does with just its 30 stocks. That said, from time to time a narrative arises that the future belongs to a handful of companies that are at the forefront of where the world is headed. As recently as June 30th, the top 5 U.S. stocks accounted for approximately 24% of the S&P 500’s value and the other 495 stocks accounted for the remaining 76%.9 The last time a small group dominated this much was 1999 just prior to the dot.com bubble bursting See Item 1 below.

Item 1: Market Concentration

I was fortunate enough to have attended a lecture by NYU Business School professor Aswath Damodaran four years ago in which he discussed the sky-high valuations of Tesla and other market favorites. He argued that each company is valued both on what it is as a business and also on what it might become. Very little of the value of McDonalds or Waste Management is based on what they might become, but a considerable amount of Tesla’s value is tied up in what technologies Elon Musk may pioneer in the future. Nvidia’s current value places a very high premium on what artificial intelligence will ultimately achieve. All of this is fine, but there is a certain risk to valuing a company on what it might become. It might never fulfill its potential, either because of management missteps, the emergence of a superior competitor or technology, or because the opportunity itself was never that great. Even when you are right about the long term you can be very wrong in the short term – Microsoft stock fell over 72% between the end of 1999 and the end of February 2009; Tesla over 73% from November 4, 2021 to January 3, 2023. Stock with this kind of volatility should be components in a portfolio, but not the bulk of portfolios.

The S&P 500 equal weighted Index was up 3.83% last quarter and 6.71% year-to-date. I do not argue that you should have just as much Alaska Air or Ralph Lauren or Hasbro 10 in your portfolio as you do Apple or Amazon, but I know you cannot run an economy on technology alone.

A benchmark can be a useful guide to performance, but it should not push you into making unwise investment decisions. The Standard & Poors 500 Index reflects the weighted investment performance of 500 of the largest U.S. companies, but it does not tell you how you should personally be positioned. Increasingly it is the default investing option for those who don’t have the time or discernment to look into market fundamentals. A popularity contest if you will. Inevitably, some of today’s most favored stocks will become tomorrow’s beehive hairdos or parachute pants.

When we put together the core of an investment portfolio, we want future growth potential for sure, but we also want some stability and predictability as well. Mostly we want companies whose products and services are not going to be obsolete in five or ten years, and whose cash flow generation is more steady than episodic. That is why we diversify even when concentrating one’s assets in one area would have generated a greater return. One witticism about diversification, the idea that spreading out one’s assets into different, less-correlated baskets reduces risk, is that “Diversification means always having to say you’re sorry.”11 It also means never having to say “Sorry about your retirement funds. You’ll have to go back to work.”12

[1] Per Morningstar workstation, as is the information on the Dow and S&P 500. ↩︎

[2] According to the S&P 500 equal weighted index ↩︎

[4] All foreign performance information per MSCI via Morningstar Workstation ↩︎

[5] All bond performance information per Bloomberg via Morningstar Workstation ↩︎

[6] Though I did say that one shouldn’t get too aggressive. ↩︎

[7] September has the worst average return of any month over the last ten and twenty years, according to tradethatswing.com ↩︎

[8] A dual share class structure gives a certain class stock greater voting rights than others. ↩︎

[9] For more on this see Barron’s Magazine, July 10, 2023 “The S&P 500 is Now a Tech Fund” by Lauren Foster. ↩︎

[10] All three found in the bottom dozen or so stocks in the S&P 500. ↩︎

[11] Brian Portnoy, Forbes Magazine, March 9, 2015. ↩︎

[12] Diversification does not guarantee investment returns and does not eliminate the risk of loss. Diversification among investment options and asset classes may help to reduce overall volatility. ↩︎

DISCLOSURE

Past performance is no assurance of future results. Trademark Financial Management, LLC (“Trademark”) is a registered investment adviser with its principal place of business in the State of Minnesota. Trademark and its representatives are in compliance with registration requirements imposed upon investment advisers by those states in which Trademark operates. Trademark may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration. This newsletter is limited to the dissemination of general information pertaining to its investment advisory/management services. Any subsequent, direct communication by Trademark with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. A complete list of all recommendations will be provided if requested for the preceding period of not less than one year. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities in this list. Opinions expressed are those of Trademark Financial Management and are subject to change, not guaranteed and should not be considered recommendations to buy or sell any security. For information pertaining to the registration status of Trademark please contact Trademark at (952) 358-3395 or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov).

For additional information about Trademark, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein or by calling 952-358-3395. Please read the disclosure statement carefully before you invest or send money. Any reference to a chart, graph, formula, or software as a source of analysis used by Trademark Financial Management staff is one of many factors used to make investment decisions for your portfolio. No one graph, chart, formula, or software can in and of itself be used to determine which securities to buy or sell, when to buy or sell them, or assist any person in making decisions as to which securities to buy or sell or when to buy or sell them. Any chart, graph, formula, or software used is limited by the data entered and the created parameters. The data was obtained from third parties deemed by the adviser to be reliable. Nonetheless, the adviser has not verified the results and cannot be assured of their accuracy.

Summary

The markets experienced as much volatility last quarter as we normally see in a full year, but it was mostly to the upside. Several of 2022’s most underperforming assets saw a remarkable comeback, most notably bonds and technology stocks. Largely this was a result of investors’ willingness to overlook persistent short-term inflation and the Federal Reserve’s determination to rein in that inflation whatever that may cost. Many investment professionals believe the Fed should stop raising rates as it is now clear that at least some banks were not able to successfully navigate the 475 basis-point (4.75%) of increases we’ve already had. Additional rate hikes risk making this situation even worse.

U.S equities rose 7.18% last quarter. The average S&P 500 stock rose just 2.93% but the market cap-weighted index was pulled higher by a handful of technology stocks like Meta and Nvidia. The Nasdaq composite soared 17.05%! Much of this occurred in the last three weeks of the quarter as the market figured that the crisis in the financial sector meant the Federal Reserve had to pause. The Fed, as it turned out, thought otherwise. The money that went to technology tended to come out of three main sectors. One obviously was financial stocks after Silicon Valley Bank collapsed. Financials lost -2.27% last quarter, but that was still better than both the energy (falling oil prices, -4.37%) and the utilities sectors (-3.12%).

International developed markets outperformed the U.S. market. MSCI EAFE recorded an 8.02% quarterly gain. Breaking this down, Europe led the way with a 10.56% return, helped by cheaper relative valuations, lower-than-feared energy costs, and the return to a positive interest rate environment. Japan rose 6.19%, led by the appointment of a new leader of the Bank of Japan. Emerging markets rose just 3.96%. China’s re-opening is expected to provide a boost to the rest of Asia and to Latin America, but we really didn’t see much of that last quarter and we might not until later this year.

Bond yields declined last quarter on hopes that the Federal Reserve would adopt a more dovish policy in the wake of the banking crisis. The U.S. bond index finished 2.96% higher, slightly less than high yield’s 3.66% increase. Even short-term bonds were able to add 1.28%. Foreign bonds were aided by a modestly weaker dollar and slightly better-than-expected economic conditions.

Commodities fell more than -3% last quarter, depending on the basket used. Falling energy prices were largely responsible. Gold, on the other hand, rose just under 8%. There are a number of possible explanations, including financial fears tied to the banking situation or perhaps concern about the coming debt ceiling circus negotiations.

Activity

Perhaps surprisingly, given the degree of volatility last quarter, we actually made very few adjustments. The more prices move back and forth, the easier it is to believe that any individual surge or drop is noise and not an important signal. For example, a dollar invested in the Nasdaq three years ago would have grown to $2.05 by year-end 2021 only to fall below $1.35 in both October and December of last year. It’s just under $1.65 today. In the context of January 2022 $1.65 seems cheap (as it is almost 20% lower than $2.05), but in the context of the 65% gain from April 2020 it still seems quite expensive. We believe we are in a “sideways” market right now, so we are not inclined in most cases to buy areas showing relative strength; we just don’t think the strength will last.

We should note that we have been willing to lock in yields on Treasury securities with yields in excess of 4.5% when market conditions have allowed. That has come to be a significant part of the fixed income component of portfolios for many of you. A 4.6% one year note only gives you 1.15% on a quarterly basis but the principal is guaranteed. After last year, having some of the return “locked in” just seems to make sense.

Outlook

The market expects three things – a mild recession, for the Fed to “pivot” from raising rates to cutting them, and for “growth” stocks to outperform. The Fed insists it has no plans to cut rates. Growth stocks have surged anyway whenever conditions have changed in such a way as to make a Fed pivot seem more likely – weaker retail sales or industrial production or home sales perhaps, or in mid-March it was the Silicon Valley Bank debacle. Eventually, some economic report, such as the employment, inflation, and housing prices, comes out stronger than expected which throws cold water on the pivot argument. As a result, the Fed hikes rates again. Growth stocks then sell off in disappointment. This is a “chase your tail” game and we’re going to be patient and not get caught up in it.

Corporate earnings declined in the 4th quarter of 2022 and they are expected to decline this quarter and next quarter as well. Simple math says that as long as earnings are declining, stock prices are getting more expensive, and time is not on your side. Over the long term, I am very confident that earnings as a whole will rise. They always have in the past, and the system is not broken. It is just a question as to whether investors can continue to see past the near term weakness.

If you have the fortitude to stay the course as annualized S&P 500 earnings fall from $228 to $217 to $208 to $199 (for example) before bottoming out and recovering to perhaps $220, $243, and then $265 by the end of 2024, then it makes obvious sense to hold on here – maybe even add if stock prices dip too far. My experience, however, is that investors tend to lose their nerve at some point as conditions continue to deteriorate. I just don’t think the next big bull market will begin from S&P 4100 (where we are today); I believe it will require a better value proposition (cheaper prices) or a drastically altered economic landscape in which earnings growth takes off like a rocket. The latter seems highly unlikely given the Fed tightening cycle and the recent bank failures. We can, however, continue to avoid any meaningful sell-off as long as investors remain relatively confident. The linchpin of that confidence is a near-term Fed pivot – investors won’t sell if they believe the catalyst to higher prices is close at hand. This is what we have to keep our eyes on.

Commentary – In a Trading Range You Do Things Differently

“Bull” markets behave in a classic way – a stock will go from $60 to $80 and then to $100 and above. The key for an investor during periods like this is to determine which parts of the investment universe are making that journey the fastest and look for a factor that is driving them that you can exploit. Maybe it’s that a particular market segment in the right industry, maybe that segment is boosting dividends or announcing share buybacks. An investor just needs to identify the catalyst fueling higher prices, and then believe that force is continue. Again, during typical bull markets corporate profits, and profit margins, are growing such that the “runway” for favorable conditions tends to be long. Occasionally there will be hiccups and adjustments will be necessary, but in general the trend is your friend and the best way to goof up and hurt your performance is to overthink it.

At the end of the economic cycle, however, the economy gets tired. Too much credit has been extended to non-worthy borrowers and interest rates have to be raised in order to purge the system of excesses so that a new expansionary phase can begin. During these periods the runway is short; stocks do not make new high after new high as they do during bull markets. They correct investors’ overenthusiasm by selling off, then they gradually work back toward their old highs only to fail to make new highs and sell off again. This is what is known as a trading range. Buying momentum in a trading range environment will not work; it will only lead to disappointment.

As noted above, corporate profits are falling today as the Federal Reserve’s tightening efforts are beginning to bite. Recessions typically begin about a year after the last Federal Reserve interest rate hike, and new bull markets tend to begin before the recession technically ends. It should be noted that the Fed hasn’t stopped hiking yet, so the bull market watch clock hasn’t even started ticking.

We’ve had economic environments somewhat similar to this one before. The ones I’m thinking of are the late 1980s and 2001 pre-9/11. In 1986 plunging oil prices created a speculative fever that led to a 35% spike and crash in 1987. Markets traded “choppily” in 1988 and 1989 as speculative excesses were wrung out. Similarly, we had a tremendous dot.com boom in 1999 partially fueled by the Federal Reserve dumping reserves in the system in case there was a system shutdown tied to Y2K. The rapid withdrawal of those reserves in early 2000 led to the dot.com crash that year and then choppy sideways trading in 2001. This go-round, the government and the Fed threw money at the economy to avert a broad economic collapse and market crash in 2020 tied to Covid-19 and largely kept the spigots open through 2021. 2022 was our “crash”, but I expect it to take at least another year of back and forth for the current excesses to be wrung out.

Sector performance courtesy of S&P per Morningstar

Bond returns from Bloomberg via Morningstar. Commodities and Gold returns from Dow Jones via Morningstar.

Growth stocks tend to perform better when interest rates fall (to the extent that interest rates reflect inflation expectations) because the lower inflation is, the less a dollar earned in the future needs to be discounted from $1.00 to reflect purchasing power loss. Growth stocks derive more of their value from expected future earnings than value stocks (which are mostly valued on net present value).

DISCLOSURE

Past performance is no assurance of future results. Trademark Financial Management, LLC (“Trademark”) is a registered investment adviser with its principal place of business in the State of Minnesota. Trademark and its representatives are in compliance with registration requirements imposed upon investment advisers by those states in which Trademark operates. Trademark may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration. This newsletter is limited to the dissemination of general information pertaining to its investment advisory/management services. Any subsequent, direct communication by Trademark with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. A complete list of all recommendations will be provided if requested for the preceding period of not less than one year. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities in this list. Opinions expressed are those of Trademark Financial Management and are subject to change, not guaranteed and should not be considered recommendations to buy or sell any security. For information pertaining to the registration status of Trademark please contact Trademark at (952) 358-3395 or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov). For additional information about Trademark, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein or by calling 952-358-3395. Please read the disclosure statement carefully before you invest or send money. Any reference to a chart, graph, formula, or software as a source of analysis used by Trademark Financial Management staff is one of many factors used to make investment decisions for your portfolio. No one graph, chart, formula, or software can in and of itself be used to determine which securities to buy or sell, when to buy or sell them, or assist any person in making decisions as to which securities to buy or sell or when to buy or sell them. Any chart, graph, formula, or software used is limited by the data entered and the created parameters. The data was obtained from third parties deemed by the adviser to be reliable. Nonetheless, the adviser has not verified the results and cannot be assured of their accuracy.

Trademark Financial Market Update – March 2, 2023

I am inclined to see the stock market as a tug of war between bullish (upward) and bearish (downward) impulses. During a bull market, the upward impulses drive us to new highs whereas the downward ones always fizzle out at a level higher than the previous downward impulse. In a bear market, just the opposite would be true. Today we are in neither. December’s failure to generate a lower low followed by January’s surge above November’s high suggests that at least for the time being the bear market is over. That said, one modestly higher high and one modestly higher low does not scream trend change. If the mid-August high around 4315 were to be broken through, then I believe we can talk about being in a bull market again.

At the very least, every impulse needs to fulfill a minimum objective or else it becomes suspect. The recent downturn took us under 4000 on the S&P 500 and under its 50-day moving average, so even though we’re less than 5% off of highs so far, it does not count as a failed breakdown (which would have bullish implications). That said, it has failed to meaningfully reverse the very sharp outperformance of growth over value in January which itself has bullish implications. Thus, while the balance of technical indicators are neutral right now, I’d lean to the bullish side.

Changing over to the fundamental side, I am less optimistic. The yield curve is inverted and becoming more so, and the trend of interest rates is higher. In an environment where the supply of goods and labor is more constrained than it was in the 2010s, and demand is greater, it is difficult to believe that consumer prices will both fall and stay at lower levels absent a full-blown recession (which I don’t see right now). Earnings are estimated to have fallen -4% year over year (the bulk of 4th quarter reports are already in). If estimated 2023 earnings are in the $215 range, today’s S&P 500 at 3985 implies a P/E of 18.5 – historically rich for a 4%+ inflation environment. Let’s put fundamentals and valuation in the mildly bearish camp.

If there were a sector I expected to do well in this environment it would be financial services – more specifically, banks. Their cost of deposits is low as savers are still generally willing to accept fairly meagre rates while they (banks) can turn around and receive much higher rates lending it out. In order not to like banks you would have to believe this unusually large funding spread is going to be offset by pending large loan losses, and I just don’t see that. What the market does think it wants today is semi-conductors. Partially due to AI, and partially due to the idea that the current drop in chip demand (relative to supply) won’t last, this area has done very well (19%) this year. Consider me a skeptic, because in my view those stocks have run too far ahead of fundamentals.

I am also surprised at how much investors seem to hate “risk-off” industries like utilities and health care so far this year. Higher interest rates are a headwind for utilities because it increases the cost of their debt and it makes their dividends less valuable, but to offset these costs they will likely ask regulators if they can charge customers higher rates and receive this request. Although investors have thus far punished managed care and pharma stocks, I don’t see a bear case for them that would result in continued underperformance.

Lastly, I feel ambivalent about foreign stock and bonds right now. They had a very good 4 month move due to the weaker dollar but as the dollar has firmed up this month, foreign outperformance has stalled. Not reversed, just stalled. Europe is still doing slightly better than the U.S., but Asia has been underwhelming. Too much in the latter area depends on guessing what China is going to do.

Disclosure

Past performance is no assurance of future results. Trademark Financial Management, LLC (“Trademark”) is a registered investment adviser with its principal place of business in the State of Minnesota. Trademark and its representatives are in compliance with registration requirements imposed upon investment advisers by those states in which Trademark operates. Trademark may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration. This newsletter is limited to the dissemination of general information pertaining to its investment advisory/management services. Any subsequent, direct communication by Trademark with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. A complete list of all recommendations will be provided if requested for the preceding period of not less than one year. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities in this list. Opinions expressed are those of Trademark Financial Management and are subject to change, not guaranteed and should not be considered recommendations to buy or sell any security. For information pertaining to the registration status of Trademark please contact Trademark at (952) 358-3395 or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov). For additional information about Trademark, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein or by calling 952-358-3395. Please read the disclosure statement carefully before you invest or send money. Any reference to a chart, graph, formula, or software as a source of analysis used by Trademark Financial Management staff is one of many factors used to make investment decisions for your portfolio. No one graph, chart, formula, or software can in and of itself be used to determine which securities to buy or sell, when to buy or sell them, or assist any person in making decisions as to which securities to buy or sell or when to buy or sell them. Any chart, graph, formula, or software used is limited by the data entered and the created parameters. The data was obtained from third parties deemed by the adviser to be reliable. Nonetheless, the adviser has not verified the results and cannot be assured of their accuracy.

Summary

First of all, we are happy to report that the fourth quarter of 2022 was a positive one for both stocks and bonds. This allowed the year to finish well above the September lows. The S&P 500 closed with a 7.56% quarterly gain, reducing its full year loss to -18.11%. Value industries such as energy and materials gained 22.86% and 15.05% respectively, while growth industries like technology rose just 5.14% and consumer discretionary lost -9.09%.

Maybe the biggest surprise last quarter was the strength in foreign stock markets. Left for dead due to the Ukraine conflict, fears about energy prices in the coming winter in Europe, Covid lockdowns in China, and other concerns, international stocks blasted upward by 17.34%. There is a lesson here in terms of how profitable it can be to invest in an area when one’s fellow investors have all but written it off. Europe has had a very mild winter so far, such that its aggregate energy usage is much less than forecast, enough so that analysts are moving away from their earlier forecasts of a deep recession. China has recently lifted all Covid-related mobility restrictions, which has produced a bit of a boom in consumer- and raw material-related stocks.

Bonds also gained during the quarter. True, their gain of 1.87% made just a minor dent in the -15% plus losses sustained in the bear market from November 30, 2021 to October 24, 2022, but it looks increasingly like a major bottom was made on that day. After a decade of receiving yields so tiny that they didn’t nearly compensate for taxes and inflation (low as it was at that time), bond investors can now obtain yields of over four percent on government bonds and six percent or more on many high quality corporates. The dollar’s decline during the quarter finally revived international bonds, which had struggled mightily over the past three years. They rose 2.58%, according to Morningstar, after falling more than 14% over the previous three quarters.

Alternative assets had a mixed quarter. Gold rose 9.45% on investors’ belief that central banks would have to ease up on interest rate hikes as inflation itself was peaking. On the other hand, energy prices turned lower which in turn dragged down the returns of managed futures funds by an average of 3.43%. Real estate-related interval funds, which had completely sidestepped the nearly 30% correction in publicly-traded real estate companies in the first nine months of the year, belatedly began to reflect negative effects of rising rates.

Activity

After bottoming out in terms of international exposure in the third quarter of 2022, we began to add back to it last quarter as the U.S. dollar made a significant top in October. The dollar is the key to the performance of “risk assets” outside of the United States – as cheap as foreign assets had become, the dollar needed to stop rising in order for those assets to move up. Like a beach ball held underwater, once the dollar trend finally turned lower, foreign asset prices shot upward. Outside of tax-related balancing of gains and losses, most of the changes made during the quarter were either driven by the reversal in the dollar or the desire to by less “tech-heavy” in our growth funds..

By October, bond yields had risen to levels that we had not seen in years, so we also did some “bottom-fishing” in the long-term end of the bond market. As inflation slows, yields come down and allow longer term bonds to make a nice profit. It is always hard to buy securities when they are down 25%-30% year-to-date (as they were back then), but I’m already wishing I had purchased larger positions.

Outlook

As this is being written, the primary driver in the markets is the deceleration in inflation. This has led to speculation about when the Federal Reserve will stop raising rates (and in fact when they might pivot to cutting them again). This is inherently a bullish conversation, standing in direct opposition to the one we were having a few months ago which was essentially “how high does the Federal Reserve need to get interest rates in order to break the upward trend in inflation”? The falling inflation narrative will be constructive to stock and bond prices as long as it lasts. That said, we are heading into corporate earnings reporting season in a couple of days. This is not likely to change the positive short-term dynamics in the bond market, but it certainly could for stocks if companies start warning about lower sales and higher costs. Let’s hope that doesn’t happen.

Commentary – “Di-Worse-ification”

The second half of the 20th century was the heyday of investment theory. Before this time investors tended to be either speculators or income collectors. They did not look at their holdings as a “portfolio”, so they did not think about how much or how little each security correlated to the others. As a result, the values tended to rise and fall in tandem (at different rates, of course). The thought that one might achieve better results by combining securities with different attributes such that they did not all rise or fall at the same time just did not occur to most investors. Then William Sharpe, Jack Treynor, Harry Markowitz, Robert Merton, Fischer Black, and others came along and turned portfolio management into a science. No longer would portfolio managers get away with buying a few promising stocks and/or bonds and hoping for the best; now there were multiple tools to assess risk-adjusted return (and advanced knowledge of mathematics would be required). These Nobel laureates taught us that markets were more or less efficient, and for a little while it actually seemed like they were.

The “Dot.com Crash” in 2000 was the first in several blows the brave new world of investment theory has suffered this century. Clearly markets couldn’t be efficient if Cisco Systems could trade above $150 in March 2000 and under $40 less than eighteen months later. Diversification, the idea that risk-adjusted returns could be improved by putting a lot of different “eggs” into one’s investment “basket” (versus loading up on the type of egg judged to be the best), similarly looked to have been disproved lately as U.S. stocks outperformed during both good and bad times over the past decade. Noting this, a clever pundit coined the term “De-worse-ification”.

A review of asset class performance over the past twenty-five years, however, shows that performance for any particular asset tends to go through multi-year periods of better and worse returns. During that period large company U.S. stock performance were first or second of the ten major asset categories every year from 1995 through 1998, then they didn’t crack the top five of ten in ANY of the next twelve years. Large U.S. stocks jump back into the top five (second) in 2013 and remain in the top five every single one of the next nine years (2013-21) before breaking the streak last year. Similarly, foreign developed and emerging markets each land in the top four every year between 2003 and 2007, but thereafter are only found in the top four together once (2017).

The lesson here is to think about diversification not as something that adds value during a particular market decline but over one’s investment lifetime. An asset class can be out of favor and underperform for the better part of a decade. In fact, some diversification models include gold and oil as additional asset classes to those referenced above. Gold and oil can and have remained out of favor for very long periods of time (close to twenty years), but when they “pop”, they can provide very exciting returns – as oil did last year.

What diversification does do, reliably, is compress the range of potential returns. It takes the highest possible return (100% of one’s in the best asset) out of the equation, but it also removes the worst. Mathematically, it averages out better than the midpoint between the best and worst asset classes, so it is what we call “risk-efficient”. That is why despite it not working well from time to time, diversification remains a foundational principal of investment management.

A little more background might be helpful. The period from 2017 though 2021 was exceptionally frustrating as an investment manager. Large cap U.S. stock had fallen out of favor in the decade of the “oughts”. By 2012, they were priced very reasonably provided the economy did not lapse back into recession. It didn’t, and 2013 through 2016 provided very nice returns for investors (especially in technology). By 2017, U.S. stocks were no longer cheap, and yet they added another 22% that year. In 2018 interest rates began to rise as they typically do late in an economic expansion. Every single asset class suffered in 2018 relative to 2017. That said, large cap U.S. stocks remained a top asset class even with a slight loss; all other equity classes posted double-digit losses. Then they rose another 31% in 2019.

When Covid hit in early 2020 and markets sold off worldwide, it looked like we were finally going to see the kind of correction that would bring large company stock returns back into line with other asset classes, allowing investment returns to be more evenly distributed. In fact, just the opposite happened. Technology’s leadership over the rest of the market only intensified post-Covid, and the performance advantage of U.S. stocks over their foreign counterparts went from large to unprecedented. The extreme out-performance of a handful of American technology companies distorted everything. Any investment professional with a cursory knowledge of history and mathematics knew this couldn’t last, but when and how would it stop?

Finally, last year, the “tech fever” fully broke. The end was foreshadowed in 2021 when the most speculative, loss-making companies began declining in earnest, but it took an inflation spike, a regional war, an oil spike, and 400 basis points of Federal Reserve tightening to finally burst the bubble. Every one of those high-flyers is now more than 25% off its all-time high while energy, consumer staples, and industrial stocks tend to be less than 5% from their highs. Even international stocks are only 15-20% off their all-time highs. Diversification seems to be working once again. Investment theory, as taught by the CFA Institute and the College of Financial Planning, is actually describing the real world again.

I am very excited about the opportunities I have as an investment manager today because all asset prices are much more reasonable. Unlike the entire decade of the 2010s I can get fair compensation relative to inflation for holding a bond. With tech fever having ended, I am not being pushed to over-weight portfolios to an industry sector that I know cannot fulfill the unrealistic growth and profit expectations the market has attached to it. There are many attractively priced stocks outside the United States that are finally starting to attract interest.

At Trademark Financial Management we run diversified portfolios. Not because they are guaranteed to produce better returns (they aren’t) but because diversification provides better risk-adjusted returns in an environment where one does not know what the future will bring in terms of asset class performance. We look for trends, and we monitor changes in the narratives that drive stocks and bond prices at any given time. We will overweight, modestly, those parts of the market that have relative strength compared to other areas, those parts of the market that are more reasonably priced than other areas, and those that fit the narrative currently driving market movements. On the other hand, we will underweight (again modestly) those areas that are either expensive or being de-emphasized by the current narrative. Over the long term, that should lead to above average performance.

Standard and Poors 500 Index, per Morningstar Workstation

S&P Dow Jones Indices, per S&P Global, December 30, 2022.

MSCI EAFE, per Morningstar Workstation

Because you are essentially asking, “Are stock prices going to go up sooner or later”? The previous question was essentially, ”For how long does the stock market need to decline”?

DISCLOSURE

Past performance is no assurance of future results. Trademark Financial Management, LLC (“Trademark”) is a registered investment adviser with its principal place of business in the State of Minnesota. Trademark and its representatives are in compliance with registration requirements imposed upon investment advisers by those states in which Trademark operates. Trademark may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration. This newsletter is limited to the dissemination of general information pertaining to its investment advisory/management services. Any subsequent, direct communication by Trademark with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. A complete list of all recommendations will be provided if requested for the preceding period of not less than one year. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities in this list. Opinions expressed are those of Trademark Financial Management and are subject to change, not guaranteed and should not be considered recommendations to buy or sell any security. For information pertaining to the registration status of Trademark please contact Trademark at (952) 358-3395 or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov). For additional information about Trademark, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein or by calling 952-358-3395. Please read the disclosure statement carefully before you invest or send money. Any reference to a chart, graph, formula, or software as a source of analysis used by Trademark Financial Management staff is one of many factors used to make investment decisions for your portfolio. No one graph, chart, formula, or software can in and of itself be used to determine which securities to buy or sell, when to buy or sell them, or assist any person in making decisions as to which securities to buy or sell or when to buy or sell them. Any chart, graph, formula, or software used is limited by the data entered and the created parameters. The data was obtained from third parties deemed by the adviser to be reliable. Nonetheless, the adviser has not verified the results and cannot be assured of their accuracy.

Summary

As hard as it would have been to believe, three months ago, that the stock and bond market could both continue to decline, they both did. U.S. stocks gave up an additional -4.88% while bonds moved -4.75% lower. Through the first three quarters of 2022, stocks are off -23.87% and bonds stand at -14.61%. A 60/40 mix of stocks and bonds, long considered the benchmark for diversified portfolios, would have lost -20.17%. There are only two years, since records have been kept, that a blended stock and bond portfolio has lost -20% or more; 1931 (the heart of the Great Depression) and 1974 (Arab oil embargo). This kind of year only comes around every 40-45 years or so. If it is any consolation, both 1931 and 1974 were followed by two consecutive years of 15%+ returns.

Figure 1: 60/40 Portfolio Returns 1926-2022

Small cap stocks peaked on November 8, 2021 and through September 30th, 2022 had declined a little over -32%. Compare this to the S&P 500, which didn’t peak until this past January 4th and is only down -25.23%. Small caps only shed -2.19% last quarter, so it’s possible that they are bottoming earlier and will lead the next bull market; they certainly lagged during the last one (especially after September 2018). Energy has been the only stock sector of refuge this year, gaining over 40% and even that sector suffered a -24.5% plunge between June 8th and September 26th. 2022 has seen nice but short rallies followed by relentless grinding declines to lower lows in almost every sector, including those that traditionally hold up during periods of stock market weakness (utilities and real estate) or inflation (gold/precious metals).

International stocks lost another -9.36% last quarter, leaving them off -27.09% year-to-date. Latin America, which is heavy in natural resources-related companies, rose last quarter and is modestly ahead over the first nine months of the year. Japan is down close to -27% this year but that is mostly due to a plunge in the yen versus the dollar; in yen terms the Nikkei is close to flat on the year. Elsewhere, however, things are just not good. Asia (aside from Japan and India) is suffering from the continued contraction of the Chinese economy and Europe is being clobbered by Russia’s Ukraine war and its own mismanagement (looking at you, England).

Rising bonds yields have served as the main catalyst for this year’s poor market performance. Bonds continue to suffer from several headwinds:

1. Inflation continues to surprise on the upside. Goods prices are moderating, but wages and housing costs are still rising greater than 5%.

2. World central banks are selling dollar-based securities (bonds) to limit the rise in the dollar against their currency. Remember, the price of a bond moves inversely to the yield on that bond.

3. The U.S. Federal Reserve is selling bonds to banks to take money out of circulation, thereby cooling economic activity (and hopefully inflation as well). On the plus side, yields on the benchmark 10-year Treasury Bond are now over 4%, so savers are finally beginning to get rewarded. The fact that bonds now yield more than twice as much as stocks provides a good rationale for believing that bonds will be attractive once the Fed stops raising rates. We are already seeing institutions selling stocks to buy bonds because they can lock in actuarily acceptable returns. While 2022 has seen the worst high quality bond sell-off in over forty years, it seems very likely that the worst is now over.

ActivityWe have been very active this year because markets have been very difficult. In many model portfolios, we have hedged the dollar exposure in international bonds and in part of our international stock portfolios. We also have added commodity exposure, bond alternatives and interval funds in some portfolios. We now have very little exposure to the most volatile area of the stock market, small cap growth funds. The goal has been to get defensive, but not so defensive we wouldn’t participate if there was a meaningful rally in risk assets.

Figure 2: Stock and Bond Returns. Very rare to see both stocks AND bonds doing so badly at the same time. In down years, bonds almost always act as “ballast” to cushion the blow from falling stock prices.

OutlookAt this point, it seems fairly certain that 2022 is going to be a “red marble” year. The hope around mid-year was that inflation would show signs of moderating in the third quarter of 2022 such that the Federal Reserve could be done tightening by year-end. Anticipating this, investors would begin to buy stocks. In fact, this did happen between late June and mid-August. Unfortunately, the July Consumer Price Index report, released in mid-August, was just too strong. It forced Fed Chairman Powell to make a very hawkish speech the next week at the annual Fed conference in Jackson Hole, Wyoming, which crushed the 2022 hopes of both bond and stock investors. He said the Fed is not going to stop raising interest rates in 2022, and furthermore they do not expect to begin to lower them any time in 2023. This was not what investors wanted to hear.

This creates a dilemma. U.S. stocks are not expensive now if one believes that the economic downturn the Fed is engineering in order to bring down inflation is not going to be either deep or long-lasting. In fact, if corporate earnings decline modestly into 2023 as margins contract but begin to rebound in the second half of next year, the market may rally. It should be noted that there are two key “ifs” in the last two sentences, and we aren’t even considering Russia, China, and potential inclement weather affecting consumption, so there are no guarantees. That said, we finally have hit price levels on many companies for which a patient investor today is likely to make a nice return by 2025 or 2026. Investors just have to have the fortitude to hold on, because the next few months are likely to contain more negative surprises than positive ones.

The good news is that big declines are often followed by big gains (though this should not be taken as a guarantee):

Commentary – Beware the V

We receive a tremendous amount of research every day concerning the economy, the stock and bond markets, interest rates, real estate, global geopolitical developments, trading strategies, and more. Sometimes I receive something so useful I immediately think, “that’s going in the Commentary”. Such was the case with this chart I was recently sent by Goldman Sachs. It shows the average performance of the S&P 500 stock index during a bear market. As you can see, the decline begins with a long meander, such that one doesn’t even think about it as a bear market. Some market sectors are performing well, while others have rolled over.