U.S. stocks added another 2.6% last quarter, bringing its full year return to 17%.1 It was a rather subdued quarter compared to the previous three quarters, and once again international stocks performed substantially better. Investors felt a little more cautious about technology stocks last quarter as concerns grew as to whether the hundreds of billions being spent on artificial intelligence (AI) would have the kind of payoff that big tech stock prices implied. As the focus shifted to industries that would benefit from AI (versus those that were producing it), health care emerged as a winner. Utilities and real estate continued to struggle because both sectors are seen as beneficiaries of lower long-term interest rates. While the Federal Reserve cut short rates twice, this did not do much to lower mortgage rates.2 Investors are trying to figure out the economy in which profits are rising quite nicely but this isn’t leading to more job creation.3

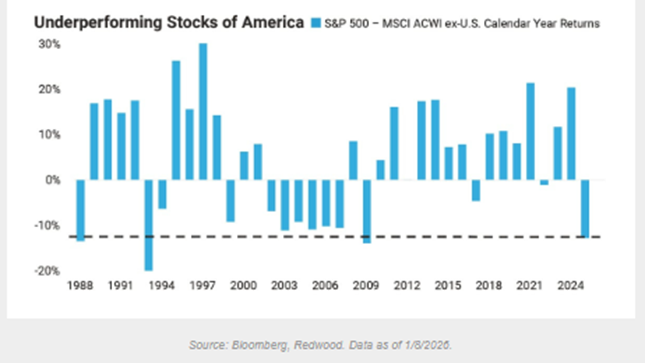

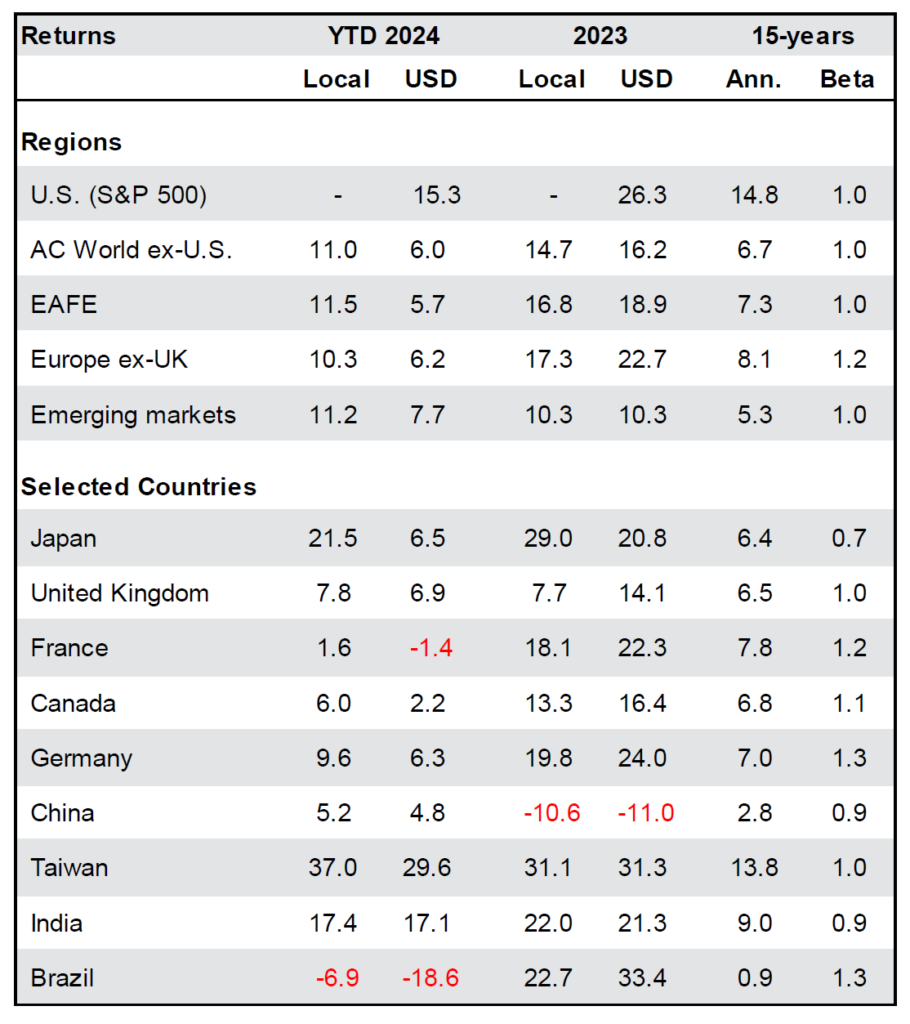

For several years we have been saying that international stocks are cheaper, but until this past year that really didn’t matter. For U.S. investors, the strength of the dollar tended to cancel out much of the gains foreign markets made in the local currency. Last year both factors needed to produce better foreign stock returns occurred; the dollar fell against most foreign currencies and local market stock performance was strong enough to close some of that huge fifteen-year performance gap. Overall, foreign stocks rose 3.8% last quarter and 33.1% for the full year.4 Brazil, South Korea, Taiwan, Germany and Canada all rose more than twice our 17% gain; India was the real laggard amongst major markets last year.

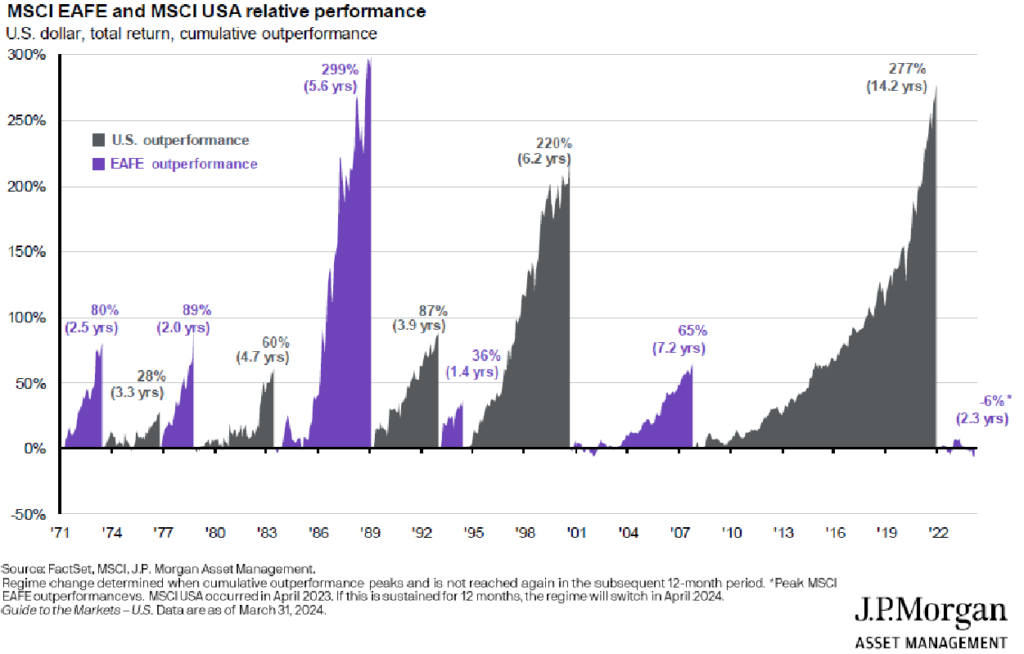

The U.S. stock market had a great run against foreign markets for dollar-based investors, but it looks like it may be over. Relative investment performance is a metric that tends to trend, and the trend appears to have reversed.

Bonds rose 1.2% during the quarter to end the year up 7.2%. This was the first year since 2020 that investors weren’t better off in short maturity bonds. There was optimism about long term rates coming down in September and October, but that had dissipated by December. The biggest profits on the bond side were in emerging market bonds, which rose about 3% last quarter and 14% for the year. Money market returns were over 4.2% last year, but their annualized rate slipped under 4% by the end of the year.

Commodities were the strongest area of the market last year, specifically the metals sector. Industrial metals rose 15.8% last quarter on increased demand for copper and aluminum for constructions. Precious metals rose 15.6% last quarter and 68% for the year due to unprecedented demand for both gold and silver, having mostly to do with global political instability. Crypto- currency had made some inroads in terms of replacing gold in recent years, but bitcoin’s small loss in 2025 showed that when you really need an alternative to the U.S dollar, only gold will do.

Activity

We reallocated portfolios in late September and October because we felt that the market had successfully navigated the seasonally weak late August through late September period without incident and would reward more aggressive positions to the end of the year. We did not get the kind of “Santa Claus rally” that you get in some years. Defensive industries (utilities, real estate) did underperform those that are more economically sensitive (industrials, transportation), with the exception of health care. We also worked hard from Thanksgiving to the end of the year to minimize capital gains. Since stocks rose by 17% and bonds increased by 7%, there simply weren’t enough losses to offset those gains, so we did our best with what was available. I guess lack of losses is a good problem to have. The other issue we encountered was the rapid increase in the price of gold. We established a 2% position in portfolios many years ago for those occasional periods of instability. It seemed like all of 2025 was a period of instability, and those 2% gold positions become 3-4%. We have been taking profits into strength, with our feeling now that gold should not exceed 3% to 3.5%. At some point that degree of volatility can work against you.

Outlook

Any advisor will tell you that there is never any shortage of opinions about where the market is headed. At the beginning of any year, every major investment firm has a webinar in which they give you their prediction for the year. If they are a product shop (i.e. they sell investments), the predictions will almost certainly be bullish on both stocks and bonds. On the other hand, if they sell research or analytics, they are often overly pessimistic because they feel that negativity makes them seem smarter. We are making no prediction about investment returns this year because we just see too many wild cards out there. Not least of these is the geopolitical and economic objectives of the United States, which seem to change on a weekly basis.

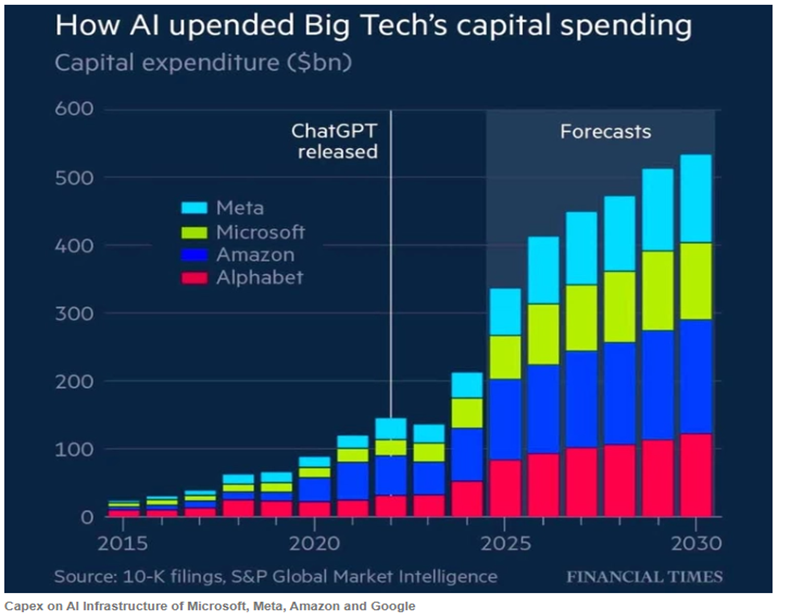

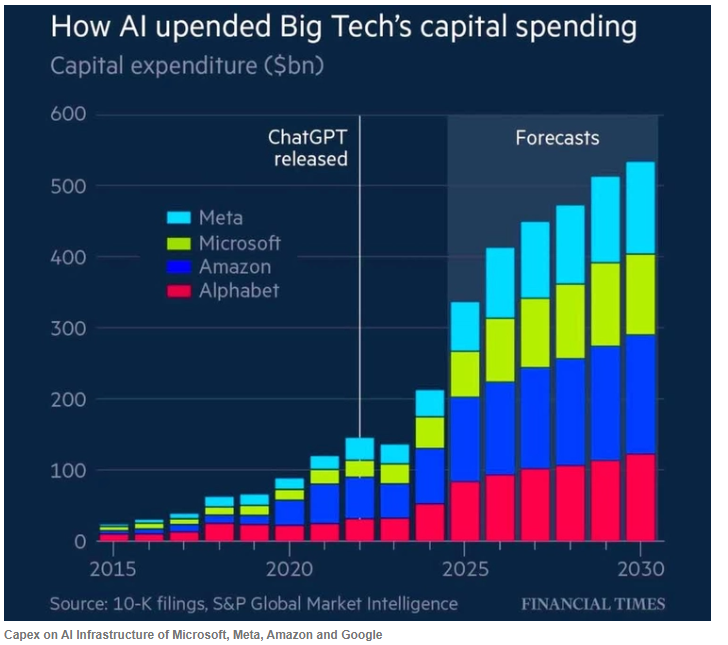

Aside from that, AI spending and future revenues are the biggest unknowns in the market right now. AI is already being used widely in industry to boost productivity, but there is no “killer app” yet. Access to AI at this point is free for writing and editing purposes and is available at a reasonable subscription price for larger entities. That said, it has not reached the “I’ve got to have it whatever it costs” stage that binds you to it and gives providers a large, growing, and reliable income stream.5 This could be a problem because many technology and related stocks are priced on the assumption that the high margin application stage will be reached. Even if AI becomes essential, it’s uncertain whether we could produce enough electricity to power all of the things we expect it to do. So, in a sense we are building the proverbial bridge as we are crossing it.

If this chart is true, then the big technology hyper-scalers will be spending so much money building out their AI programs that they won’t be able to afford much in the way of dividend increases or share buybacks. Stock prices have already begun to reflect concern.

On the positive side, some parts of the market (small caps, emerging markets) that haven’t moved much over the past ten years (and are therefore reasonably priced) have been doing well lately. If there is widespread disappointment with technology profitability, money will probably rotate into other sectors as long as the general economy holds up. Interest rates are the key. If the ten-year note can stay around 4%, we’ll probably be okay this year.

Commentary – Random Thoughts

In the absence of one unifying theme for this commentary, I’d like to present a few quotes and ideas and charts that have interested me lately.

Michael Cembalest is an investment strategist for J.P. Morgan whose research and ideas are “must reading” among financial professional these days. A lot of what I know about the opportunities and challenges of AI are from his writings. There are two things he has written recently that I have noted:

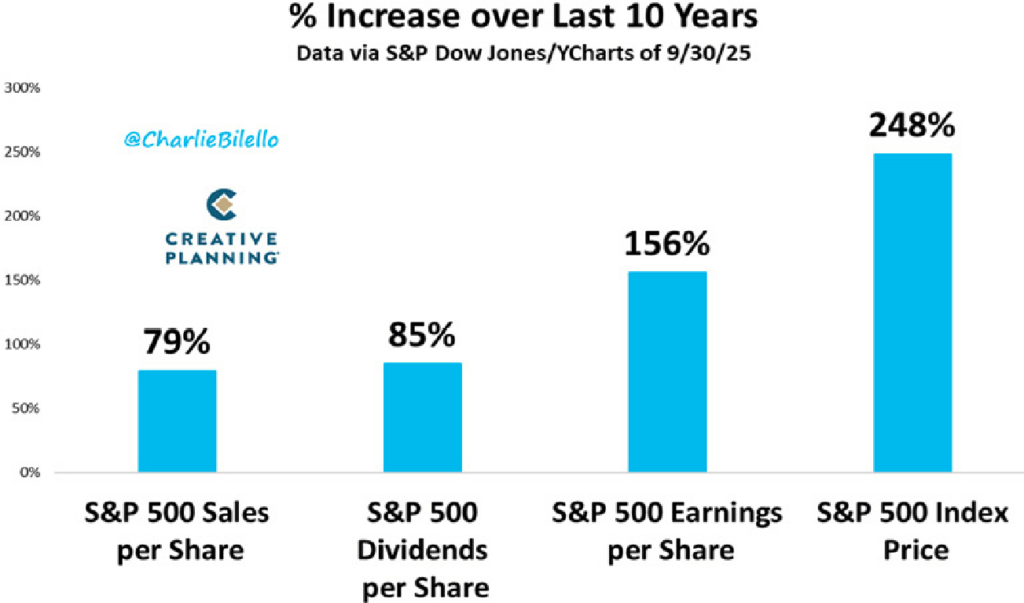

1. “US technology price-to-earnings-growth ratios are only 1-3 times in recent years. In the dot.com era stock prices were 4-8 times expected annual earnings growth”.6 In other words, we have not maxed out at all what investors might pay at the top of the cycle.

2. “After a correction, ask “what could go right” rather than obsessing over factors that led to the selloff. And when markets are highly concentrated and near all-time highs, the right question to ask is “what could go wrong”.7 He is saying that there aren’t enough people thinking today about what might go wrong because every sell-off since 2011 has been an opportunity to buy. At some point, the market will cry wolf and there really will be a wolf.

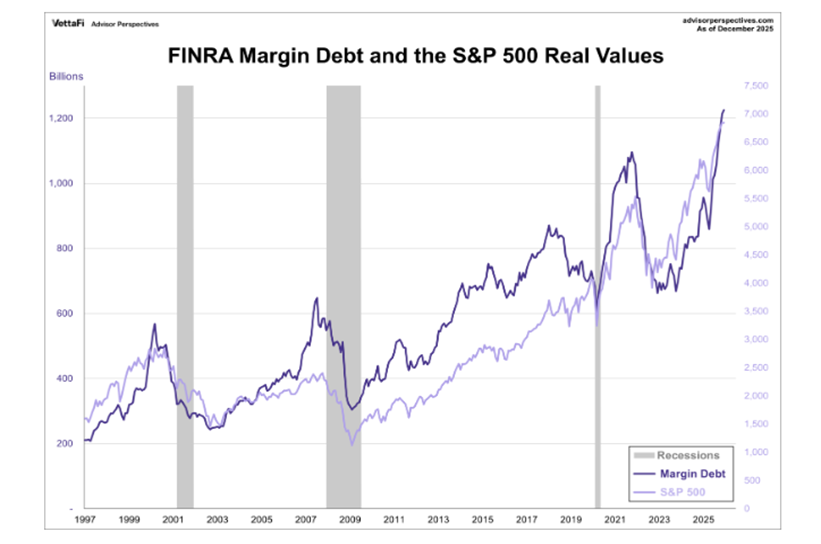

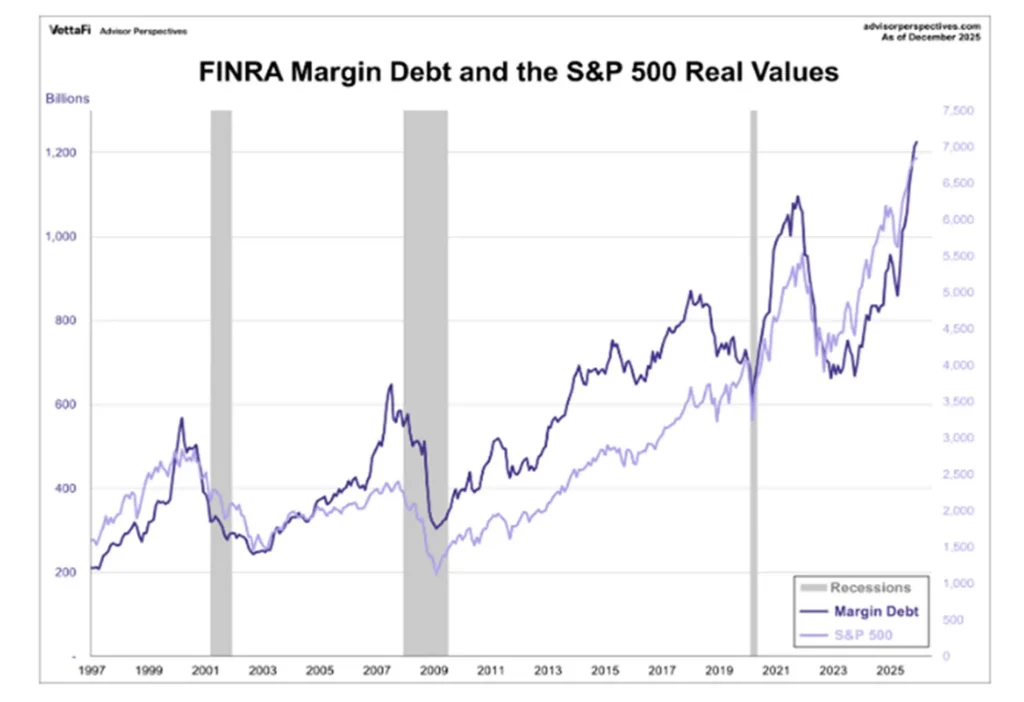

Margin Debt is a measure of how aggressive (leveraged) stock market investors are in aggregate. As you can see, we are at all-time highs. This doesn’t mean we can’t go higher, but it does suggest that the current advance is pretty far extended. When this measure starts to fall, often a recession is not far behind.

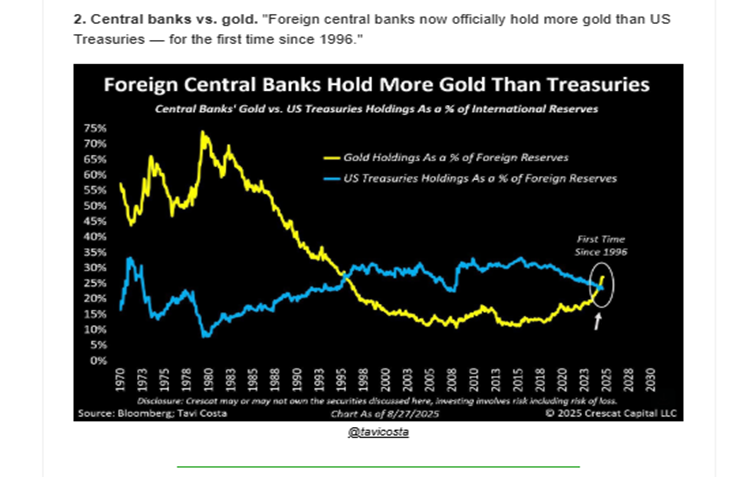

One of the reasons for the big surge in gold prices is the surge is buying by foreign central banks. Why have they been buying gold and selling their U.S. Treasuries? Every country has its own reasons, but China has been trying to diversify away from the dollar since the mid-2010s when the trade war with the U.S. intensified. The sharp move in recent years has to do with widespread fears that the U.S. might seek to punish any country that did not fall in line behind it, much as it punished Russia economically after the Ukraine invasion and Iran before that.

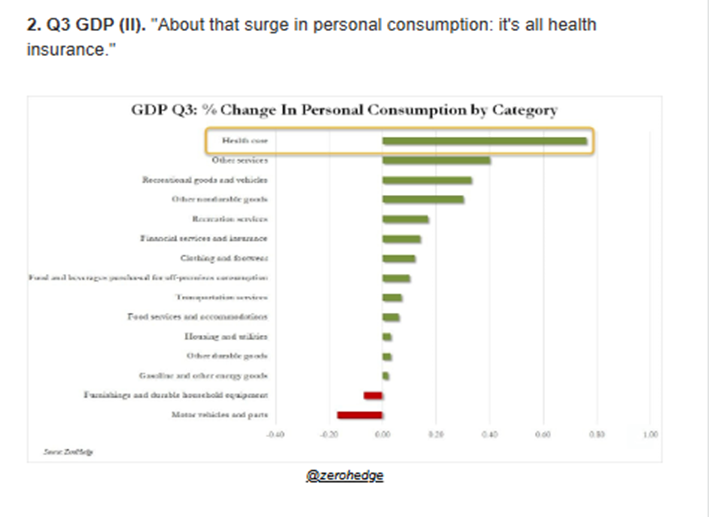

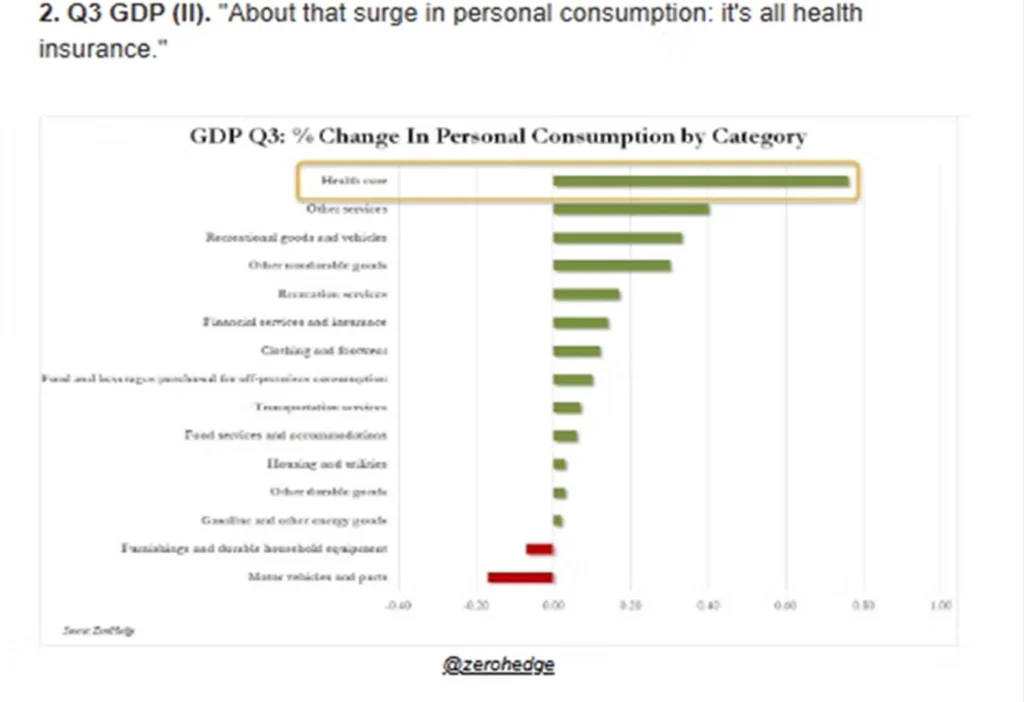

The economy was not as strong last year as it appeared. Largely, GDP rose because we spent more for health insurance.

[1] S&P 1500 U.S. Stock Composite, via Standard & Poors. ↩︎

[2] Because mortgages tend to be tied to it, the ten-year U.S. Treasury is seen as the key to the housing sector. ↩︎

[3] Except in health care, but those are primarily lower wage jobs tied to taking care of senior citizens. ↩︎

[4] JPMorgan Asset Management, Guide to the Market 1Q26. In U.S. dollar terms. ↩︎

[5] Like the iPhone, for instance, or Google. You could use a different phone or search engine, but the network effects of both of these was overwhelmingly powerful. ↩︎

[6] Michael Cembalest, JP Morgan – Eye on the Market ↩︎

[7] Michael Cembalest, JP Morgan – Eye on the Market ↩︎

DISCLOSURE

Past performance is no assurance of future results. Trademark Financial Management, LLC (“Trademark”) is a registered investment adviser with its principal place of business in the State of Minnesota. Trademark and its representatives are in compliance with registration requirements imposed upon investment advisers by those states in which Trademark operates. Trademark may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration. This newsletter is limited to the dissemination of general information pertaining to its investment advisory/management services. Any subsequent, direct communication by Trademark with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. A complete list of all recommendations will be provided if requested for the preceding period of not less than one year. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities in this list. Opinions expressed are those of Trademark Financial Management and are subject to change, not guaranteed and should not be considered recommendations to buy or sell any security. For information pertaining to the registration status of Trademark please contact Trademark at (952) 358-3395 or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov). For additional information about Trademark, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein or by calling 952-358-3395. Please read the disclosure statement carefully before you invest or send money. Any reference to a chart, graph, formula, or software as a source of analysis used by Trademark Financial Management staff is one of many factors used to make investment decisions for your portfolio. No one graph, chart, formula, or software can in and of itself be used to determine which securities to buy or sell, when to buy or sell them, or assist any person in making decisions as to which securities to buy or sell or when to buy or sell them. Any chart, graph, formula, or software used is limited by the data entered and the created parameters. The data was obtained from third parties deemed by the adviser to be reliable. Nonetheless, the adviser has not verified the results and cannot be assured of their accuracy.

Summary

U.S. stocks added another 2.6% last quarter, bringing its full year return to 17%.1 It was a rather subdued quarter compared to the previous three quarters, and once again international stocks performed substantially better. Investors felt a little more cautious about technology stocks last quarter as concerns grew as to whether the hundreds of billions being spent on artificial intelligence (AI) would have the kind of payoff that big tech stock prices implied. As the focus shifted to industries that would benefit from AI (versus those that were producing it), health care emerged as a winner. Utilities and real estate continued to struggle because both sectors are seen as beneficiaries of lower long-term interest rates. While the Federal Reserve cut short rates twice, this did not do much to lower mortgage rates2. Investors are trying to figure out the economy in which profits are rising quite nicely but this isn’t leading to more job creation.3

For several years we have been saying that international stocks are cheaper, but until this past year that really didn’t matter. For U.S. investors, the strength of the dollar tended to cancel out much of the gains foreign markets made in the local currency. Last year both factors needed to produce better foreign stock returns occurred; the dollar fell against most foreign currencies and local market stock performance was strong enough to close some of that huge fifteen-year performance gap. Overall, foreign stocks rose 3.8% last quarter and 33.1% for the full year.4 Brazil, South Korea, Taiwan, Germany and Canada all rose more than twice our 17% gain; India was the real laggard amongst major markets last year.

The U.S. stock market had a great run against foreign markets for dollar-based investors, but it looks like it may be over. Relative investment performance is a metric that tends to trend, and the trend appears to have reversed.

Bonds rose 1.2% during the quarter to end the year up 7.2%. This was the first year since 2020 that investors weren’t better off in short maturity bonds. There was optimism about long term rates coming down in September and October, but that had dissipated by December. The biggest profits on the bond side were in emerging market bonds, which rose about 3% last quarter and 14% for the year. Money market returns were over 4.2% last year, but their annualized rate slipped under 4% by the end of the year.

Commodities were the strongest area of the market last year, specifically the metals sector. Industrial metals rose 15.8% last quarter on increased demand for copper and aluminum for constructions. Precious metals rose 15.6% last quarter and 68% for the year due to unprecedented demand for both gold and silver, having mostly to do with global political instability. Crypto- currency had made some inroads in terms of replacing gold in recent years, but bitcoin’s small loss in 2025 showed that when you really need an alternative to the U.S dollar, only gold will do.

Activity

We reallocated portfolios in late September and October because we felt that the market had successfully navigated the seasonally weak late August through late September period without incident and would reward more aggressive positions to the end of the year. We did not get the kind of “Santa Claus rally” that you get in some years. Defensive industries (utilities, real estate) did underperform those that are more economically sensitive (industrials, transportation), with the exception of health care. We also worked hard from Thanksgiving to the end of the year to minimize capital gains. Since stocks rose by 17% and bonds increased by 7%, there simply weren’t enough losses to offset those gains, so we did our best with what was available. I guess lack of losses is a good problem to have. The other issue we encountered was the rapid increase in the price of gold. We established a 2% position in portfolios many years ago for those occasional periods of instability. It seemed like all of 2025 was a period of instability, and those 2% gold positions become 3-4%. We have been taking profits into strength, with our feeling now that gold should not exceed 3% to 3.5%. At some point that degree of volatility can work against you.

Outlook

Any advisor will tell you that there is never any shortage of opinions about where the market is headed. At the beginning of any year, every major investment firm has a webinar in which they give you their prediction for the year. If they are a product shop (i.e. they sell investments), the predictions will almost certainly be bullish on both stocks and bonds. On the other hand, if they sell research or analytics, they are often overly pessimistic because they feel that negativity makes them seem smarter. We are making no prediction about investment returns this year because we just see too many wild cards out there. Not least of these is the geopolitical and economic objectives of the United States, which seem to change on a weekly basis.

Aside from that, AI spending and future revenues are the biggest unknowns in the market right now. AI is already being used widely in industry to boost productivity, but there is no “killer app” yet. Access to AI at this point is free for writing and editing purposes and is available at a reasonable subscription price for larger entities. That said, it has not reached the “I’ve got to have it whatever it costs” stage that binds you to it and gives providers a large, growing, and reliable income stream.5 This could be a problem because many technology and related stocks are priced on the assumption that the high margin application stage will be reached. Even if AI becomes essential, it’s uncertain whether we could produce enough electricity to power all of the things we expect it to do. So, in a sense we are building the proverbial bridge as we are crossing it.

If this chart is true, then the big technology hyper-scalers will be spending so much money building out their AI programs that they won’t be able to afford much in the way of dividend increases or share buybacks. Stock prices have already begun to reflect concern.

On the positive side, some parts of the market (small caps, emerging markets) that haven’t moved much over the past ten years (and are therefore reasonably priced) have been doing well lately. If there is widespread disappointment with technology profitability, money will probably rotate into other sectors as long as the general economy holds up. Interest rates are the key. If the ten-year note can stay around 4%, we’ll probably be okay this year.

Commentary – Random Thoughts

In the absence of one unifying theme for this commentary, I’d like to present a few quotes and ideas and charts that have interested me lately.

Michael Cembalest is an investment strategist for J.P. Morgan whose research and ideas are “must reading” among financial professional these days. A lot of what I know about the opportunities and challenges of AI are from his writings. There are two things he has written recently that I have noted:

1. “US technology price-to-earnings-growth ratios are only 1-3 times in recent years. In the dot.com era stock prices were 4-8 times expected annual earnings growth”.6 In other words, we have not maxed out at all what investors might pay at the top of the cycle.

2. “After a correction, ask “what could go right” rather than obsessing over factors that led to the selloff. And when markets are highly concentrated and near all-time highs, the right question to ask is “what could go wrong”.7 He is saying that there aren’t enough people thinking today about what might go wrong because every sell-off since 2011 has been an opportunity to buy. At some point, the market will cry wolf and there really will be a wolf.

Margin Debt is a measure of how aggressive (leveraged) stock market investors are in aggregate. As you can see, we are at all-time highs. This doesn’t mean we can’t go higher, but it does suggest that the current advance is pretty far extended. When this measure starts to fall, often a recession is not far behind.

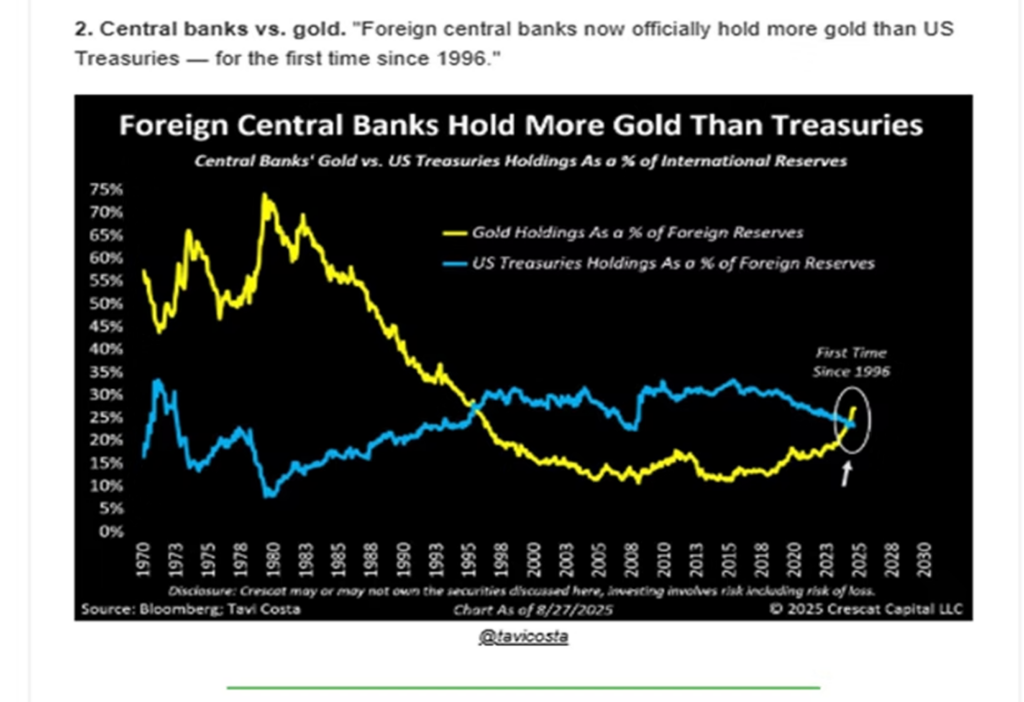

One of the reasons for the big surge in gold prices is the surge is buying by foreign central banks. Why have they been buying gold and selling their U.S. Treasuries? Every country has its own reasons, but China has been trying to diversify away from the dollar since the mid-2010s when the trade war with the U.S. intensified. The sharp move in recent years has to do with widespread fears that the U.S. might seek to punish any country that did not fall in line behind it, much as it punished Russia economically after the Ukraine invasion and Iran before that.

The economy was not as strong last year as it appeared. Largely, GDP rose because we spent more for health insurance.

Diclosure

Past performance is no assurance of future results. Trademark Financial Management, LLC (“Trademark”) is a registered investment adviser with its principal place of business in the State of Minnesota. Trademark and its representatives are in compliance with registration requirements imposed upon investment advisers by those states in which Trademark operates. Trademark may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration. This newsletter is limited to the dissemination of general information pertaining to its investment advisory/management services. Any subsequent, direct communication by Trademark with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. A complete list of all recommendations will be provided if requested for the preceding period of not less than one year. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities in this list. Opinions expressed are those of Trademark Financial Management and are subject to change, not guaranteed and should not be considered recommendations to buy or sell any security. For information pertaining to the registration status of Trademark please contact Trademark at (952) 358-3395 or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov).

For additional information about Trademark, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein or by calling 952-358-3395. Please read the disclosure statement carefully before you invest or send money. Any reference to a chart, graph, formula, or software as a source of analysis used by Trademark Financial Management staff is one of many factors used to make investment decisions for your portfolio. No one graph, chart, formula, or software can in and of itself be used to determine which securities to buy or sell, when to buy or sell them, or assist any person in making decisions as to which securities to buy or sell or when to buy or sell them. Any chart, graph, formula, or software used is limited by the data entered and the created parameters. The data was obtained from third parties deemed by the adviser to be reliable. Nonetheless, the adviser has not verified the results and cannot be assured of their accuracy.

[2] Because mortgages tend to be tied to it, the ten-year U.S. Treasury is seen as the key to the housing sector. ↩︎

[3] Except in health care, but those are primarily lower wage jobs tied to taking care of senior citizens. ↩︎

[4] JPMorgan Asset Management, Guide to the Market 1Q26. In U.S. dollar terms. ↩︎

[5] Like the iPhone, for instance, or Google. You could use a different phone or search engine, but the network effects of both of these was overwhelmingly powerful. ↩︎

[6] Michael Cembalest, JP Morgan – Eye on the Market ↩︎

[7] Michael Cembalest, JP Morgan – Eye on the Market ↩︎

Summary

The stock market rally continued, with the S&P 500 adding another 8.1% last quarter to bring its year-to-date gain up to 14.8%. Once again, technology was the leader, as its 13.2% quarterly gain was driven by sky-high aspirations for growth in the artificial intelligence trade(AI) sector. The only declining sector was consumer staples (think Pepsi and Procter & Gamble), which posted a -2.4% loss. The AI boom is mainly lifting technology stocks (especially those that produce the semiconductor chips that power the search for greater intelligence), but it’s also the boosting the utility stocks that provide the power, the real estate stocks that provide the land where data centers are built, the industrial stocks that build the plants and cool them so they don’t overheat, and the financial stocks that raise the money for all of this. There is a certain gold rush mentality in the stock market right now, which is exciting but also increasingly concerning.

Emerging markets outpaced both U.S. stocks and foreign developed markets stocks last quarter. China was especially strong as its government provided significant support to its technology sector. Knowing that cutting-edge semiconductor chips from Nvidia would no longer be available because of trade restrictions, China has gone “all-in” on producing its own. Many of the best performing foreign markets this year have been in the emerging area – Vietnam, South Korea, Poland, and Peru – are each up more than 50%. That’s why you diversify.

Bonds added another two percent last quarter, bringing their year-to-date return to 6.1%. When interest rates started to soar in early 2022, investors found that they were better off in money market funds than in bond funds because the latter was more volatile yet returned less because of inflation. That hasn’t really been the case over the last 12 months; the promise of interest rate cuts has invigorated the bond market as money market yields have fallen. High-yield bonds have risen 7.2% this year, nicer than Treasuries, but maybe not enough extra yield for the added risk. So far this year, global bonds have continued to be the top performers. Emerging market debt rose another 4.3% last quarter and is up close to 11% year-to-date. Municipal bonds have been the weakest sector of the bond market this year, but they finally began to perform in August and finished the quarter up 3.1%.

All the above paled in comparison to the stellar gains from the gold sector. Gold bullion soared 16.4% last quarter due to several factors, including global central bank demand and fears about U.S. interest rates and trade policy. Gold mining stocks, which can be considered leveraged investments tied to gold price movements, experienced a 43.8% increase in the last quarter. Gold is a very volatile sector, so it is essential to make changes incrementally.

Activity

Risk-taking was clearly in fashion last quarter as stocks in select niches like quantum computing, uranium mining, and cryptocurrency staking made large moves. There isn’t much one can do in an environment like this – we are not going to chase stocks in companies that are just starting up and hardly even have revenues (let alone profits). We were more interested in weeding out some underperformers (stock funds that leaned too heavily into real estate, health care, energy, or consumer staples) than making any major changes. Sometimes it pays to buy what is cheap and out of favor, but this past quarter was not such a time. On the bond side, in addition to extending the duration to benefit from declining interest rates, we also reduced floating rate exposure because lower rates mean lower yields.

Outlook

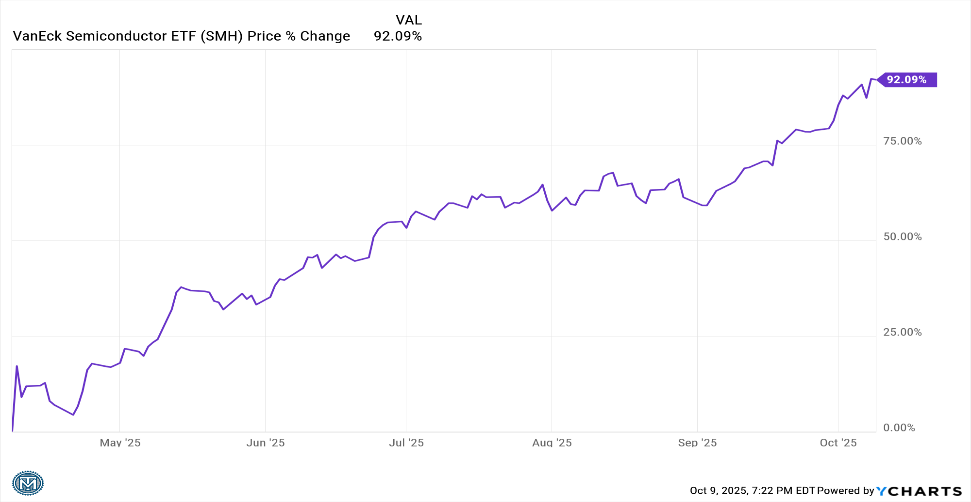

Historically, September is a difficult month for stocks. Market started to anticipate this by flattening out in mid-August, but positive interest rate news sent the market soaring again after Labor Day. I have learned over decades in this business to be nervous when investors get this ebullient, but I know I’m never get the exact timing of a market top. If one leaves the party too early, one can miss a lot. The S&P 500 has provided outstanding returns since 2012, so if one is going to go against the big technology names that lead this index, one better be very sure of both their thesis and their timing (and I am not). I just know that trees don’t grow to the sky. A couple of charts of hot sub-sectors show just how far and how fast we’ve run up:

Semiconductors are up over 92% since April 8th. They are a key component in Artificial Intelligence, but still… 92% in six months?

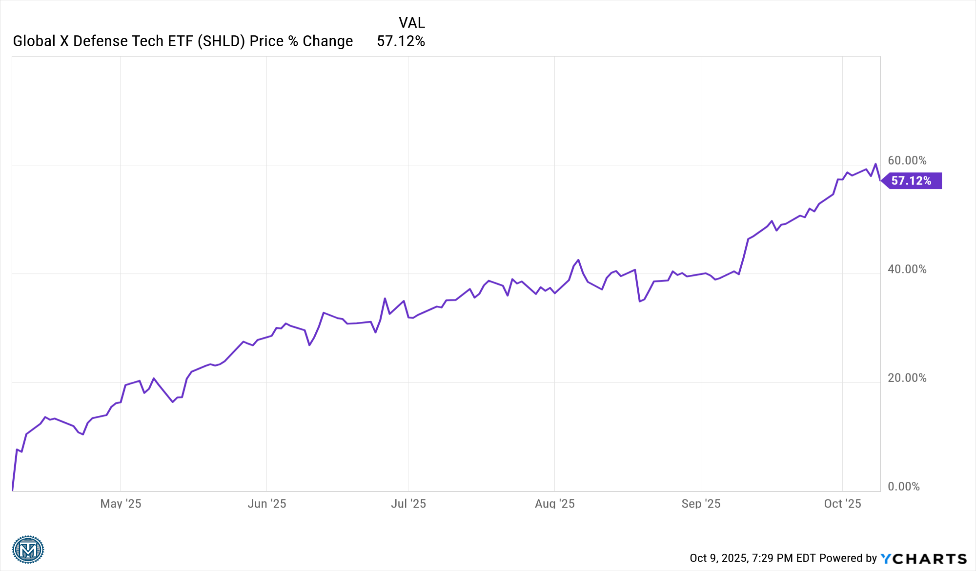

This is the defense technology sector. Up 57% in six months. The charts for gold, coal, copper, uranium, quantum computing, and digital finance and just as strong (if not stronger).

I am not averse to investing in these sectors (we already do, to some extent). In fact, I believe that the two interest rate cuts we expect this year meaningfully reduces the chance that the “tech reckoning” happens in 2025. If this sounds too bearish, remember this: the bursting of the technology bubble in 2000 led to a half-decade of great returns for the small company and financial/real estate sectors because the fallout led to sharp decline in interest rates. I’m starting to become bullish about non-technology sectors. When it comes to the financial markets, someone’s pain is often somebody else’s gain.

Commentary

Since I’ve suggested that technology may not be a leading sector going forward, I owe you a good discussion of why I feel this way. You will recall that last quarter when I described the dramatic outperformance of growth over value in recent years I did not suggest that I saw an imminent end to that.1 The stock market can and often does remain overvalued for prolonged periods of time if liquidity conditions are favorable. If investors don’t get carried away, nice gains can be had for years. However, as happens every so often, investors decided they wanted to discount future earnings all at once. Several years of anticipated AI profits in different areas of the economy were priced in. This is making it exceedingly difficult to justify what is going on without making comparisons to earlier pre-crash periods like 1987 or 1999 or 2021.

Here are my main areas of concern:

1. Valuation – A Nice Increase in Earnings Growth Has Gone a Long Way

This chart shows how the market is turning modest corporate profit increases into large price gains.

2. Relative Strength – Piling Into Today’s Winners Can Be a Risky Strategy

Relative strength is a measure of how strong the price performance of an asset is versus its peers. Theoretically, one wants to own assets that are over-performing and to avoid those that are under-performing. At a certain level of over- or under-performance, however, the trend is usually unsustainable; nothing soars or plunges forever. The market uses a measure called RSI to determine good over-performance (recognition of competitive advantage) versus dangerous over-performance (assertions that said company “owns the future”). An RSI over 75 suggests the stock or ETF is doing so much better than the overall market that a period of “consolidation” – at the very least – is likely. Wall Street has a maxim: “Pigs get fat, hogs get slaughtered” to warn against feeding too heavily at the trough, so to speak.

3. Increasingly Lower Free Cash Flow – Not All Great Businesses Today Will Be Great Businesses Tomorrow

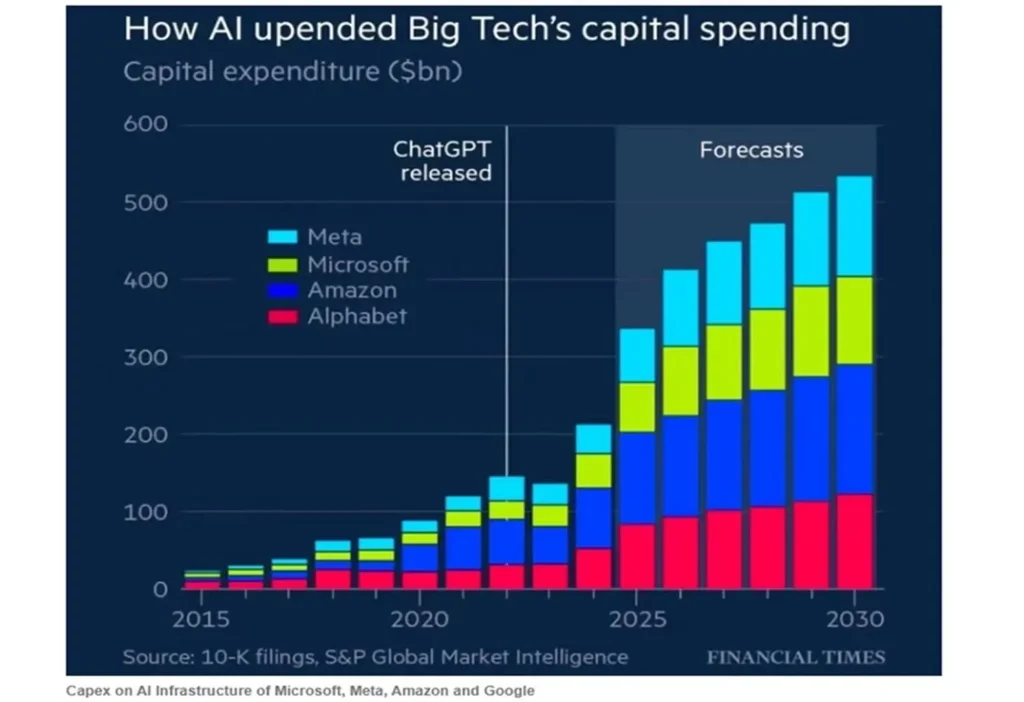

Investors typically love free cash flow, which is defined as the cash a business has left over after all expenses (including taxes and dividends) are paid, PLUS any spending required to maintain the current level of profitability (in other words, depreciation). The more the hyper-scalers (Meta, Amazon, Microsoft, and Alphabet) are forced to spend just to keep pace in the AI race with their rivals, the less they have for dividends, stock buybacks, or acquisitions.

One of the biggest attractions these stocks had up until recently was that they were huge free cash generators. As such, they commanded price-to-earnings multiples of over 30 times (while for the average stock, the P/E multiple is less than 20). If they continue to have to spend gigantic sums on their AI buildouts, they deserve lower P/E multiples.2 This implies that their current stock prices are too high.

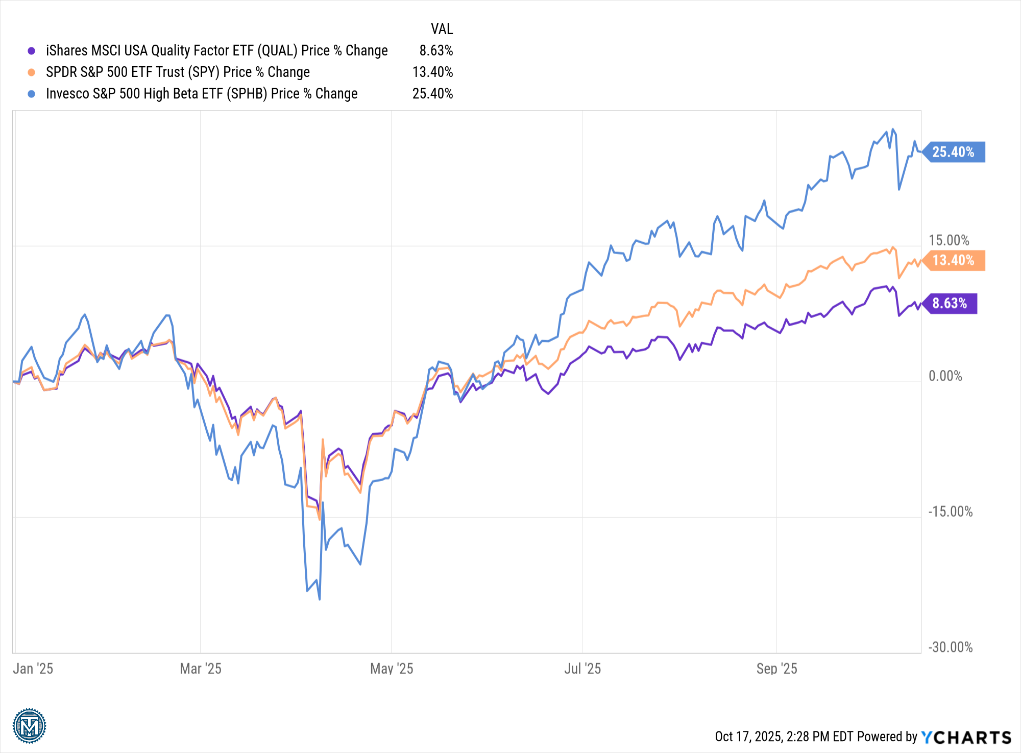

4. Quality – Lower Quality Companies Tend to Outperform Before Market Peaks

Quality, as a stock attribute, sounds like something you definitely want. It is usually defined as having a strong balance sheet, strong cash flow, and a leading position in a growing industry. Many believe that companies exhibiting these characteristics have better stock performance over time, and they are generally correct. That said, “quality” historically delivers its best performance during downturns (when poorly financed companies with declining cash flows tend to decline much, much more). While no investment manager ever says that they focus on low-quality companies, the fact is that those companies tend to perform better when speculative fever is high. Some of the biggest winners this year are either highly leveraged or very vulnerable to disruption. This has been especially true since June:

The S&P 500 is the orange (middle) line. If you extract just the riskiest companies (blue line) from that index, you earn a much better return. If you factor out the highest quality companies, you would be under-performing

5. Profit Taking Sounds Good, Realization of Taxable Gains Does Not

One of the things that made the bursting of the dot com bubble from 2000-02 so painful was that investors saw their tech portfolios lose 60-85% of their value, AND they had to pay capital gains taxes! Understandably, investors prefer to avoid taxes, so they are disinclined to sell positions that have appreciated significantly in value. What tends to happen, therefore, is that when stock prices begin to fall, investors tend to sell those positions with just modest gains and hold the ones with larger gains. This is called “profit taking”, and it is quite common. However, every decade or two, there is a significant sell-off where investors start to panic and sell more indiscriminately. The big winners tend to become big losers because those stocks and funds that didn’t see much profit-taking in the up years begin to “catch up” on the downside. These stocks have a significantly greater amount of embedded capital gains, so even down 50% or more the tax hit can be very large.

Again, all of this is offered not because I expect the tech sector to go down substantially very soon, but because I know some sort of re-adjustment is almost sure to happen and it might happen soon. We hear a lot about AI these days, but one should understand that large future sales of power, data centers, and semiconductor chips are already priced into most stocks. The kinds of things that I look for to tell me that risks are elevated – high valuations, narrowing market breadth, decreasing free cash flow, low quality leadership – are considerably more prevalent in the technology sector now than they were three months ago, which increases my nervousness. With liquidity conditions positive and interest rates set to be cut twice more this year, I think the odds of something major happing in 2025 aren’t high. I am, however, looking harder than I have in years at finding areas outside of the AI trade to shift assets to.

[2] Additionally, the new budget law recently enacted by Congress (OBBBA) allows a much slower depreciation schedule (6 years instead of 3. This change has given these firms a reported earnings benefit of 7-12% in 2025, according to TenViz. Since the actual chip and server technologies are becoming obsolete faster rather than slower, arguably depreciation schedules should have shortened rather than lengthened. ↩︎

DISCLOSURE

Past performance is no assurance of future results. Trademark Financial Management, LLC (“Trademark”) is a registered investment adviser with its principal place of business in the State of Minnesota. Trademark and its representatives are in compliance with registration requirements imposed upon investment advisers by those states in which Trademark operates. Trademark may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration. This newsletter is limited to the dissemination of general information pertaining to its investment advisory/management services. Any subsequent, direct communication by Trademark with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. A complete list of all recommendations will be provided if requested for the preceding period of not less than one year. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities in this list. Opinions expressed are those of Trademark Financial Management and are subject to change, not guaranteed and should not be considered recommendations to buy or sell any security. For information pertaining to the registration status of Trademark please contact Trademark at (952) 358-3395 or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov).

For additional information about Trademark, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein or by calling 952-358-3395. Please read the disclosure statement carefully before you invest or send money. Any reference to a chart, graph, formula, or software as a source of analysis used by Trademark Financial Management staff is one of many factors used to make investment decisions for your portfolio. No one graph, chart, formula, or software can in and of itself be used to determine which securities to buy or sell, when to buy or sell them, or assist any person in making decisions as to which securities to buy or sell or when to buy or sell them. Any chart, graph, formula, or software used is limited by the data entered and the created parameters. The data was obtained from third parties deemed by the adviser to be reliable. Nonetheless, the adviser has not verified the results and cannot be assured of their accuracy.

Quarterly Market Summary

Summary

What a turnaround! Stocks soared to a 10.9% quarterly return last quarter after President Trump reversed himself on tariffs. The “Liberation Day” tariff announcement on April 2nd caused a further 12% one-week sell-off after stocks had already fallen 8% from their February 19th highs. Investor sentiment was grim. Then, on April 9th, tariffs on foreign-made goods were largely rescinded for the time being. Stocks rose over 8% that day. Gradually, investors began to believe that their fears about inflation and recession might be overblown. They reasoned that if the administration was simply employing an aggressive negotiating tactic and never really planned on going through with tariffs of 50% and higher, maybe they aren’t as reckless as first thought. The rally really got going after Microsoft’s surprising large earnings beat on April 30th and semiconductor giant Nvidia’s assurance in May that the AI race was just getting started.

As a result, technology was the big sector winner last quarter with a 22.9% gain, but industrials also gained over 12%. Defensive industries like consumer staples (no growth), health care (RFK Jr., Medicaid cuts), and energy[1] lagged badly. U.S stocks are up 6.2% through June 30th.

Foreign stocks have done much better. In local currencies, world stocks rose 8.3% in the first half of the year. Because the U.S. dollar fell sharply as global investors shifted assets out of U.S. markets, dollar-based investors earned nearly 11% more by investing overseas. This finally provided some validation for proponents of international diversification after years of under-performance due to a strong dollar and a less advantageous industry mix[2]. Asian stocks gained the most last quarter led by China. Lessening of trade frictions were good for everybody, but the U.S. and China benefitted the most.

Bonds gained 1.2% last quarter. This is big “cool down” after a strong (2.8%) first quarter. Yields have steadied in a narrow range as investors weigh where inflation and tariff policy are going next. Non-US debt continued to benefit from a weaker dollar. Private credit and mortgage bonds also outperformed. Municipal bonds were once again the worst bond sector. They have become very cheap now, and many bond market experts are saying that this is the time to buy.

Alternative assets such as gold and bitcoin have been choppy, but both have had multiple surges to new highs this year.

Activity

The second quarter came in like a shark and went out like a kitten. The first six trading days of the quarter were wracked with tariff fears and selling, then we got the policy reversal, and then investors increasingly traded stable assets for those that had more upside potential. The key consideration for performance was how strongly one altered their positioning in March in anticipation of tariffs and how quickly one reversed those changes in April or May once the tariff scenario changed. We made moderate risk-off moves in March. By early May we had repositioned portfolios back toward risk assets, but not quite as much as if the whole thing hadn’t happened in the first place. Policy volatility continues to make this an exceptionally challenging (but not necessarily bad!) time to invest.

Outlook

Investors have learned, over the past fifteen years, that if you get a meaningful dip in stock prices you better be a buyer. The vehemence with which bearishness switched to bullishness has reinforced the notion that selling is dangerous – you are probably going to have to buy back whatever you sell, and the price may well be higher then. There are some large tariffs set to take place early next month which if implemented would likely cause stocks here and overseas to fall, but as I write this on July 17, 2025 – the stock market isn’t putting much stock into those concerns. Nobody wants to be the guy who sold out and now has egg on his face because the tariffs were just a bluff and never went into force. In essence the market is playing a giant game of chicken, so to speak. I hope it doesn’t have to blink this time.

Commentary – Warren Buffett and Michael Saylor

This seems like an appropriate time to appreciate the career of Warren Buffett, the chairman of Berkshire Hathaway and perhaps the most famous and successful investor of the past 75 years. Mr. Buffett announced in May at the annual shareholders’ meeting that he was turning the chief executive officer role over to a successor. The 94-year-old Buffett is probably most well-known for his stellar long-term returns, but to professionals his standout quality was his patience. His best returns often came from stocks that had their best years long after Berkshire first purchased them. Mr. Buffett exploited a huge behavioral weakness that investors have – the inability to accurately assess opportunities and risks that would take years instead or months to play out. Time after time he would buy stakes in strong companies that were facing a near-term challenge, then hold them while the challenge was overcome and the stock returned to its upward trajectory. A less appreciated but also important behavioral skill he possessed was the ability to avoid being drawn in by short-term market fads. He would rather let cash accumulate on Berkshire’s balance sheet than overpay for a company just because it was doing well. If you are patient, he argued, you do not have to pay top dollars for the best companies. Eventually, they will come to you. For example, he earned tens of billions of dollars for Berkshire by buying Apple stock during slumps in 2013 and 2016[1].

Warren Buffett’s approach is known as value investing, and it was the model for investing in the 20th Century. It was taught and is still taught in business schools and in the CFA program. But value investing is not the way that most investing is done today. Michael Saylor is the Executive Chairman of a company called MicroStrategy (now just Strategy), and he is a pretty good example the modern investment approach. Strategy borrows money in the bond market and uses the proceeds from its borrowing to buy bitcoins. This works because investors currently value Strategy at roughly twice the value of the bitcoins it holds. Why? Because there are many things you can do with bitcoins (including lending it to speculators for a tidy fee) and because the Trump Administration is very crypto-friendly and is likely to approve even more uses for bitcoin. Since bitcoin was invented back in 2008 it has both risen tenfold and lost two-thirds of its value several times. If Buffett’s edge is patience, Saylor’s edge is fortitude. He can psychologically withstand brutal downturns that the vast majority of investors cannot.

I bring up this comparison not because either Buffett or Saylor is a good or smart person or has the better approach but because I believe both are a product of their times. Warren Buffett was born during the Great Depression. He saw both a World War and decade long periods of time where stocks made investors less than nothing after inflation. He was influenced by Benjamin Graham’s idea of “Margin of Safety” which is decidedly a “First Principle – Don’t lose money” kind of philosophy. On the other hand, Michael Saylor started MicroStrategy in 1989. His investment career coincided with relative political stability and huge gains in the market punctuated by brief downturns in 2000-02, 2007-09, and even shorter ones in 2020 and 2022. He is a very successful investor during a climate where no matter how far asset prices fell, they always came roaring back in fairly short order. Those who picked the right asset (Apple, Nvidia, bitcoin) and went “pedal to the metal” made the most money – if they didn’t lose their nerve. Such is growth investing, and its superiority this century has been amazing.

Maybe this is how the rest of the decade will go. Maybe this is how the entire twenty-first century will go. All I can say is that I can’t believe that it will, and I cannot professionally or personally invest as if I think it will. As a student of market history (going back two centuries), I have recognized a pattern of increasingly speculative excess leading ultimately to very deep busts. The success of Strategy by itself doesn’t say anything about whether or not this is the pre-bust part of a great market cycle. Saylor may just be one of those investment geniuses that arise during both good periods and bad. But coupled with the rise in ways to outright gamble on the market, especially the explosion in options and other forms of leverage and online trading forums, I am convinced that this is one of those speculative eras that will not end well.

That said, I also know that it is beyond my ability to predict when this will happen, so getting super defensive and waiting is just not an option. I know people who have tried that.

Investing always involves risk, but today it involves more risk than usual. Not just because prices are high historically[i], but because there is a similar embrace of risk-taking and risk-takers that I’ve read about in the late 1800s and the 1920s and I lived through in the late 1990s. Moreover, this higher risk behavior is taking place at the same time as America’s policy framework is undergoing significant changes not seen since the 1930s, and at a time where corporate America is betting VERY BIG on artificial intelligence. Those are important topics whose implications I’d like to address in future Commentaries, but don’t have enough room left in this one.

So, in conclusion I’d like to thank Warren Buffett for his contributions to the field of investment analysis and management as well as to the pocketbooks of all of us who have invested over the last forty or so years. I’d also like to thank growth investors like Michael Saylor who remind investors more psychologically sympathetic to value strategies, like myself, that growth tends to perform a lot better than value when the financial and geo-political winds are at your back. I hope that this continues to be the case.

DISCLOSURE

Past performance is no assurance of future results. Trademark Financial Management, LLC (“Trademark”) is a registered investment adviser with its principal place of business in the State of Minnesota. Trademark and its representatives are in compliance with registration requirements imposed upon investment advisers by those states in which Trademark operates. Trademark may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration. This newsletter is limited to the dissemination of general information pertaining to its investment advisory/management services. Any subsequent, direct communication by Trademark with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. A complete list of all recommendations will be provided if requested for the preceding period of not less than one year. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities in this list. Opinions expressed are those of Trademark Financial Management and are subject to change, not guaranteed and should not be considered recommendations to buy or sell any security. For information pertaining to the registration status of Trademark please contact Trademark at (952) 358-3395 or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov). For additional information about Trademark, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein or by calling 952-358-3395. Please read the disclosure statement carefully before you invest or send money. Any reference to a chart, graph, formula, or software as a source of analysis used by Trademark Financial Management staff is one of many factors used to make investment decisions for your portfolio. No one graph, chart, formula, or software can in and of itself be used to determine which securities to buy or sell, when to buy or sell them, or assist any person in making decisions as to which securities to buy or sell or when to buy or sell them. Any chart, graph, formula, or software used is limited by the data entered and the created parameters. The data was obtained from third parties deemed by the adviser to be reliable. Nonetheless, the adviser has not verified the results and cannot be assured of their accuracy

[1] He was a heavy seller in 2024 at prices 6-9 times higher.

[i] Stock are statistically expensive, but that has been the case for most of the last forty years, so this fact has almost no predictive value.

[1] Energy investors always assumed that a war in the Middle East would send oil prices soaring. When the war came and went and prices were only briefly affected, the “conflict premium” declined considerably.

[2] Far more of the U.S. market is in technology, the best performing sector of the last fifteen year, than foreign markets contain.

Summary

The first quarter of 2025 started off well enough, but it deteriorated badly as the quarter came to an end. Between Election Day and Inauguration Day, the market had a lot of optimism about the new administration’s plan to aid “re-shoring” (bringing overseas manufacturing back to America). President Trump during his first term paid careful attention to how the stock market interpreted his policies, so investors naturally assumed that he would be sensitive to stock prices this time as well. So far, they have been disappointed. The stock market peaked in mid-February and has moved sharply lower ever since. Trump threatened our trading partners with large tariffs and then, despite the market’s negative reaction, followed through with them. What really roiled the markets was that the actual tariff rates proposed were both larger than expected and seemingly without any evidence of a thought-out methodology. Global financial markets – stock, bond, and currency – have reflected a movement away from the U.S. ever since[i]. US. stocks fell -4.6% during the first quarter[1]. Technology, retailing, and small cap stocks lost the most.

International stocks performed very well early on in the quarter and despite the tariff crisis still ended it with modest gains. The developed market index (MSCI EAFE) gained 7.0% and the emerging market index (MSCI EM) rose 2.9%. To some extent, foreign markets have been the beneficiaries of America’s more adversarial stance. The U.S. prospered over the years from foreign investors parking their money in our stock and bond markets. Now, having some concerns about our policies, many foreign investors are reducing their exposure here. All in all, the value of diversification really proved itself last quarter as foreign stock and bond gains somewhat offset the drag from falling U.S stocks.

U.S. bonds had a pretty decent quarter, rising 2.8% according to Bloomberg. That said, they have become increasingly volatile in recent weeks as investors try to figure out what effect tariffs will have on inflation, interest rates, our trade deficit, and the value of the dollar. After several years of outperforming government bonds, corporate bonds underperformed them in the first quarter as economic fears increased. On the other hand, after over a decade of dismally underperforming dollar-based bonds, foreign bonds had an excellent quarter. The weak dollar has really shaken things up. Perhaps the biggest beneficiary of the weak dollar and doubt over U.S. policy has been gold, because investors always need a safe-haven asset, and it doesn’t seem to be U.S. T-Bills anymore. Gold rose close to 20% during the first quarter.

Activity

The first quarter was a wild ride, especially at the end. Headlines were changing every day, many having a big impact on asset prices. Early in the quarter the market priced in de-regulation, which means faster growth but higher interest rates. That favors growth and cyclical stocks and higher-yielding bonds. As it began to be clear that the agenda for Trump’s second term was going to be a lot different than that of the first term, markets had to make some big shifts. Economic policy was not going to be conducted on the basis of whether or not the financial markets favored it; instead it was going to be more populist. That said, there was no real playbook for how to model the inflationary or deflationary impact of a trade policy in which tariff rates seemed to change daily. What we did know, however, was that the way the markets had initially positioned for a second Trump term was turning out to be completely wrong. We had to pivot toward more defensive stocks, higher quality bonds, and portfolio protection in the form of gold and other alternatives that are not as sensitive to the economy. We also needed to raise cash levels. We are still making adjustments. One notable change is that due to volatility, new funds are invested more gradually – in order to avoid buying too much on what might turn out to be an inauspicious day.

Outlook

Expect volatility. President Trump’s goal seems to be to keep everyone off balance, and he is meeting that goal so far. George H.W. Bush did not want to raise taxes in 1990, but a sharp rise in the deficit pushed the dollar down and interest rates up and forced his hand. Bill Clinton wanted to make major changes to health care and social programs in 1994, but the bond market was not having it, so he had to abandon most of his plans[2]. Sometimes markets don’t let a president do what he would like to. Usually, it doesn’t go well for the economy when presidents try to ignore markets. I believe there is room for a stock rally if this president moderates his agenda, but right now he doesn’t seem anxious to do that. Markets aren’t waiting – investors are “voting” for change by replacing the dollar with gold and the Japanese Yen, and they are trimming their stock and longer-term bond positions.

Commentary – Of Pianos, Mattresses, and Light Switches – Why it is Especially Challenging to Manage Assets in this Environment

I believe that the Trump Administration believes that the trade deficit that America has had for decades is a result of other countries taking advantage of America’s generosity, and that it isn’t fair. I believe that America consciously and purposefully ran a trade deficit. We were buying influence and giving the world an incentive to choose capitalism over Soviet or Chinese-style command economies. I believe that this influence came in handy for America after September 11th, when the U.S. called in favors and nearly everyone responded (even those that had misgivings). That said, capitalism has certainly won the economic war and revisiting our global commitments might have been in order. In his first term, President Trump complained that most European nations were not living up to their agreed-to defense financial obligations. Despite this, not much changed. Europeans knew they were not spending enough, but they also understood that they were also helping America to project its power more easily into the Middle East and Asia.

This is the political backdrop for what has occurred in the financial space since Trump has come back into the Presidency. The United States had a legitimate gripe, but is it pursuing that gripe constructively or destructively? Did it consider all the implications of blowing up the status quo? The Trump Administration resented tariffs placed on American goods as well as the non-tariff barriers many countries imposed. However, like its non-nuanced view of global geo-politics, it also had a narrow economic view. The United States of America in the 2020s is very largely a service economy. It runs a trade surplus in services with almost every country on Earth. In addition, the U.S. has its own tariffs and non-tariff barriers. This is why trade disputes are typically negotiated. It was thought to be understood that nobody really benefits from blowing up the whole framework of international trade.

The global economy is exceedingly complicated. It is very arduous and time consuming to try to change, which is why there are typically a lot of negotiations. One option Trump had was to treat the process of restructuring trade and political relationships like moving a Steinway grand piano out of a third floor studio – carefully, and with a lot of people and ropes and things. Another option was to treat it like getting rid of an old mattress – open the window and toss it out. Evidently, he is choosing the latter. Global investors have been trying to cope with this ever since.

Truthfully, we don’t know whether this bold experiment will ultimately prove to be successful, or modestly successful, or mostly unsuccessful, or disastrous. It is too soon to tell. That said, markets are always trying to anticipate future results. It would have been possible to announce the tariffs on April 2nd with a meticulous explanation as to why each country was assessed the amount it was. When that didn’t happen, markets made a downward revision to anticipated future returns. Two days later, the administration revealed a mathematical formula (with Greek letters!) to justify how much each country was tariffed. Unfortunately for them, most economists can do math with Greek letters, and they were not impressed. Side note – one can write a formula using Greek letters to explain the basic premise of American football (you need to advance the ball at least ten yards every four plays), but that doesn’t make it especially complicated. So the reveal, which was basically that we tariffed each country roughly by the percentage of our trade deficit with them, blew a hole through America’s credibility and made markets go down even more. When the 90-day reprieve was announced on April 9th, markets rejoiced to the tune of nine percent in less than three hours, but that still left us considerably short of where we began, and we still have the tariff deadline looming ahead.

All of this makes portfolio management very challenging. Typically, when an investment analyst makes a forecast, he or she is trying to assess how fast the economy is going to grow, to what extent interest rates are going to rise or fall, and most importantly what the interplay will be between the economy and interest rates. Think about this as being like a dimmer switch in your dining room – based on new input one nudges one’s expectations up or down a bit. If necessary, you have to replace a less suitable asset with a more suitable one. Now think about how tariffs impact a forecast. A 5% tariff increase affects a company’s profit margins; maybe they pass it on to their customers, maybe they have to absorb it themselves, but they want to keep the business so they pay it. A 25% tariff, on the other hand, is probably too large to absorb. If they can’t pass most of it on, they have to consider foregoing the import and telling their customer to get it from somebody else. Recently, the Trump Administration and China have raised tariffs on each other to over 100%. That is a “FORGET IT” level. Nothing (except tiny components) gets bought or sold at that tariff level. Economies start to go south very fast when trade grinds to a halt. That’s not a dimmer – that is an off switch! A portfolio in a “dark” room is going to have to be a great deal different (more conservative) than a portfolio in a lighted room.

Obviously, the value of any income stream changes dramatically when its tariff rate changes from 40% to 10%, as happened on Wednesday April 9th. There was an intraday rally of almost 9%. It is very hard to model for something like that. How does an investor respond to this kind of volatility? If you are an investor not domiciled in the United States, you can’t possibly anticipate what the U.S. President might say or do next, so you protect yourself by selling dollar-based assets. You reduce exposure to the “suddenly-not-so-safe” haven of U.S. bonds and stocks and increase your weighting of alternative safe havens like gold (up 26.5% year-to-date) or the Japanese yen (+10.5%). This is what we have seen lately.

For the last decade or so prominent investors have used metaphors like “cleanest dirty shirt”[3] to illustrate the point that however concerned one might be about America that every other country as an investment option was considerably worse. American asset outperformance became so taken for granted in recent years that “American exceptionalism”[4] was widely used in investment circles. These notions are being called into question now. Again, I don’t know how this is all going to be resolved, but I do know that I can’t put the same valuations on U.S. assets that I did in the “TINA” (There Is No Alternative) Era. U.S. assets will necessarily carry lower premiums over foreign assets than they did from 2012 to 2024. It doesn’t mean they won’t produce nice gains, but as a whole they should underperform non-US bonds and stocks. Alternatives like gold and commodities are going to have to be a larger part of portfolios as well.

In all probability, the world has now entered a new era. The word “uncertainty” has been bandied about frequently in recent weeks. The Trump Administration has an ambitious agenda to shake up global trade and politics and make them more friendly to American interests, but that is exceedingly difficult under even the best circumstances. It will require a level of diplomacy that is so far not in evidence. I am not speaking from personal conviction here, I am simply conveying the message of the markets, and so far that message has not been very favorable. As the rally on April 9th demonstrates, there is room for asset prices to improve dramatically if tariffs are abandoned, but I have no thought that going through all of this for nothing would be regarded by markets as positive either. Because of the increased levels of both volatility and uncertainty, we at Trademark believe we have to exercise more caution, at least in the short term, than we have had to in recent years. We take our responsibility as manager of your assets extremely seriously. Over the past decade, stock market sell-offs have provided very good “buy-the-dip” opportunities. I am not as confident that this is the approach to take this time.

[1] S&P 500 large company index, according to Standard and Poors. The NASDAQ Composite fell -10.3% and the Russell 2000 small cap index sank -9.5% according to Nasdaq.com.

[2] This prompted James Carville, Clinton’s political strategist, to opine that if he were ever resurrected, he’d like to come back as the bond market because then he could intimidate everyone.

[4] A laudatory phrase from 19th century French political philosopher Alexis de Tocqueville.

[i] A large part of the problem, as many in the market have stated, was that wasn’t clear why we needed to end the era of American market exceptionalism. If you look at a chart of relative performance, the U.S. was by far the largest beneficiary of the status quo over the last fifteen years or so. There is no economic policy that guarantees that absolutely everybody will do better. Clearly, many industrial jobs were lost during this time period (though far more were lost between 1985 and 2000). Congress sent money to the states many times to try to alleviate the economic pain of those who lost their jobs, but some states simply pocketed it or cut taxes (which, while nice, does nothing to help someone who isn’t earning any money).

In any event, we have begun a policy of blaming and punishing our trading partners for taking jobs we gave U.S. corporations tax incentives for moving under the Reagan, George H.W. Bush, and Clinton Administrations. Needless to say, those countries aren’t happy about it. So far, those industries most exposed to tariff concerns have fared worse than those that largely do business domestically, but even energy, which Trump promised specifically to help, has seen losses over 15% as global demand falls.

DISCLOSURE

Past performance is no assurance of future results. Trademark Financial Management, LLC (“Trademark”) is a registered investment adviser with its principal place of business in the State of Minnesota. Trademark and its representatives are in compliance with registration requirements imposed upon investment advisers by those states in which Trademark operates. Trademark may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration. This newsletter is limited to the dissemination of general information pertaining to its investment advisory/management services. Any subsequent, direct communication by Trademark with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. A complete list of all recommendations will be provided if requested for the preceding period of not less than one year. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities in this list. Opinions expressed are those of Trademark Financial Management and are subject to change, not guaranteed and should not be considered recommendations to buy or sell any security. For information pertaining to the registration status of Trademark please contact Trademark at (952) 358-3395 or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov). For additional information about Trademark, including fees and services, send for our disclosure statement as set forth on Form ADV from us using the contact information herein or by calling 952-358-3395. Please read the disclosure statement carefully before you invest or send money. Any reference to a chart, graph, formula, or software as a source of analysis used by Trademark Financial Management staff is one of many factors used to make investment decisions for your portfolio. No one graph, chart, formula, or software can in and of itself be used to determine which securities to buy or sell, when to buy or sell them, or assist any person in making decisions as to which securities to buy or sell or when to buy or sell them. Any chart, graph, formula, or software used is limited by the data entered and the created parameters. The data was obtained from third parties deemed by the adviser to be reliable. Nonetheless, the adviser has not verified the results and cannot be assured of their accuracy.

Summary

With dividends reinvested, the S&P 500 gained close to 25% in 2024, but only 2.4%1 of that came in the final three months. Stocks lost one percent in October (as is typical in the month leading into a presidential election). Stocks then rose 5.7% in November in what many market pundits referred to as the “Trump bump”, as investors looked favorably on the potential for less regulation and more merger activity. December saw the market give back almost half of that (-2.5%) as investors digested the policies of the president-elect and winced at their inflationary implications. Bonds had a fairly poor quarter (-3.1%) as interest rates rose sharply post-election. As a result, the full-year gain was cut to 1.3%. Small and mid-cap stocks are even more sensitive to interest rate movements than large caps; they rose 9% post-election, then gave almost all that back very quickly to finish the quarter with just a 0.3% advance. Interestingly enough, there was no “Santa Claus rally” during the final trading days of 2024.

The biggest losers in November’s election may have been foreign stock investors. Largely because of threatened tariffs, foreign stocks lost -7.6% in U.S. dollar terms last quarter. Weakening prospects for economic growth in both Western Europe and China also played a part. Latin America, led by Brazil, was by far the poorest-performing region last quarter. Asia also struggled as Indian stocks took a breather after strong performance earlier in the year. Europe lost close to -8% during the quarter and the “winner”, Japan, still gave back five percent. Many argue as to whether there is value to be had in investing outside the U.S. It is true that foreign markets are less expensive in terms of valuation, but the growth rates and the profit margins of their companies tend to be quite a bit lower. With a company like Taiwan Semiconductor, however, you can get a high growth rate and a high profit margin with a price-to-earnings multiple lower than the average U.S. stock. Foreign stock investors just have to be more selective, which is why we very seldom index our foreign stock exposure, and why we underweight foreign stocks versus the global benchmark.

Bonds had a rough quarter. They rose over -3% to end the year up just 1.3%. A lot of bond analysis focuses on inflation as if that were the only important factor in where bonds prices go. Another factor and one that is taking on increasing significance these days is issuance versus demand. Simply put, if you try to sell more bonds than the bond market has the capacity or interest in buying, prices are going to go down – regardless of what inflation is doing. Inflation didn’t jump last quarter but because buyer interest in financing U.S. debt declined, the U.S. government had to offer higher yields to attract borrowers. Since corporate and mortgage debt is priced as a spread over U.S. government debt (because the government is less likely to default than a private payer), everybody’s borrowing costs rose. Only those bonds where the yield is attractive (higher) relative to government bonds (yet their default risk is still low) provide good returns in this environment.

Gold and cryptocurrency had a strong year. Gold rose largely because investors worldwide sought an alternative to questionable central bank and government policies. Cryptocurrencies surged as U.S. regulators approved ETFs that hold individual crypto tokens, such as bitcoin and Ethereum. They got a further boost after the election as President Trump promised to be a big crypto advocate.

Activity

Typically, markets are quiet into an election, and afterward, a narrative emerges in terms of which industries will be winners and which will be losers under the new regime. This time, it happened, but with a twist. It wasn’t about which industries would be losers but which countries. Tariff threats dominated the post-election market environment, so most market participants (even those overseas) figured that the best thing to do was invest in the U.S. to avoid that risk. The U.S., primarily because of its economic size and military strength, has the least to lose if global trade breaks down, though everyone would be a loser to some extent. Doing the math, the prudent play for asset allocators was to reduce international exposure, both developed and emerging, relative to US equity exposure. The second part of the tariff equation is higher interest rates, further stressing bond market didn’t have to do much. We were already defensive on the bond side and therefore had a lot less to lose from rising rates.

The other portfolio management consideration we had to address was determining the appropriate amount of large-cap technology exposure. Too little and you increased the amount you under-performed the index (which held over 35% in just eight companies at year-end); too much and you introduce too much risk to the portfolio since all investment manias ultimately end. In some portfolios, we added, and in some, we subtracted. More on this in the Commentary section.

Outlook

Writing this on Friday afternoon, January 17th, it is difficult to say where we are going to go from here. At this point, the U.S. economy is fairly strong and corporate earnings are expected to post low double-digit gains. Interest rates usually determine if the market will perform better than earnings would suggest or worse. So far this year, interest rates are up a little bit, so market gains have been modest.

All that said, we are soon to see the impact of tariffs on a scale we have never seen before (if the new President’s words are to be believed). We know that tariffs did not work in the late 1800s, and we know that they did not work AT ALL after the Smoot-Hawley Act was passed in 1930. However, it could be argued that the U.S. depended more on foreign trade in the late 19th and early 20th centuries then and was not the economic powerhouse that it is now. Since Trump’s election, markets have definitely made the calculation that since America is less dependent on its trading partners, it has less to lose from a trade war. As a result, investors have shifted assets out of countries and currencies that would be vulnerable to an economic attack from the United States. As U.S. investors, we have benefitted from this shift in the short run (more demand for dollar-based assets). It remains to be seen how long the benefit lasts. Whatever we do is bound to, at some point, produce a counter-response. It is for this reason that many strategists look for the first half of the year to be stronger than the second half.

Commentary – Risk Management Amid a Possible Speculative Bubble

2024 was another strong year for the U.S. stock market so it is probably a good time to discuss market returns and portfolio returns, as well as risk tolerance and fiduciary duty. Hopefully, this will help you to understand why stock index returns can differ a lot from portfolio returns in both directions (but typically, index returns are higher when the market is up).

First of all, I would like to point out how much investing has changed over the years. One hundred years ago, even sixty years ago, most investing was done through the trust department of banks. That is where people with significant wealth put their money because banks had a duty of care that stockbrokers didn’t have. If a bank lost your money through imprudent investments, it was legally liable to you. If you lost money with a stockbroker, on the other hand, you needed to prove fraud to have any recourse. Investing got a jolt in the 1960s as the stock market soared on the back of new technologies—integrated circuits, mainframe computers, instant photography, etc. Investors got frustrated by the safe but low-yielding options offered them by banks (bonds, preferred stocks, etc.), so as they did in the 1920s when cars and radio were the big new things, they began to speculate. Ultimately, this ended in tears as well. The first oil crisis in 1973-74 was a harsh reminder that even technology can fall prey to a global economic contraction.

The tension between investing and speculating has evolved over the last fifty years. Fiduciary investing became dominated by mutual funds and then indexed exchange-traded funds (ETFs), with speculation being done through individual stocks and privately traded vehicles. Speculators had their day trading phase in the late 1990s and then moved on to leveraged ETFs, leveraged single stock ETFs, SPACs, meme stocks, cryptocurrencies, and zero day-to-expiration option contracts (0-DTE) more recently. New innovations in speculation have historically always happened just before the top of a market cycle (because at the beginning of a cycle, investors are more cautious than greedy). It seems to me that we are probably near the top of the cycle now partially because2 of all of the new speculative vehicles that have been recently introduced, but admittedly, this is a gut feeling and not something I can know for certain.

As a Registered Investment Advisor (RIA), however, I have certain legal responsibilities, and as a Chartered Financial Analyst (CFA), I have fiduciary3 and ethical requirements. I am, therefore on the investment side of the equation, not the speculative. As such, I am more like a bank than a broker. There are risks I cannot take with a client’s money, even if the client wants me to. That doesn’t mean I’m always going to be correct. Putting all of someone’s money in Apple or Tesla ten years ago was not prudent from a fiduciary standpoint; it might have resulted in a complete loss. Obviously, we now know that it didn’t – those stocks turned out to have been far more lucrative than any diversified portfolio one could have owned. Things always look clearer in hindsight.